After Covid: Japan’s Catch-Up

Better late than never. After a disappointing start to its vaccine rollout, Japan got on its feet in August, vaccinating as many as 1.58% of the population per day at the peak of the campaign. For context, the highest level of daily doses administered in the U.S. was 1.01% in April1.

Though Japan’s vaccination pace has tapered as the ranks of the inoculated builds, it’s now in that zone where anyone who wants the vaccine can easily get it. Critically, more than four out of every five seniors have been fully vaccinated, with that cohort’s proportion surpassing that of the U.S. in mid-August2. Nevertheless, the younger age groups’ vaccination rate still lags that of Western Europe and North America, though it appears a full catch-up with other G7 members should be on the docket for next month.

With Japan no longer behind on COVID-19 vaccinations, its relative investment merit falls back on traditional metrics such as valuations and the matter of whether the country’s shareholder friendliness is on the mend.

The latter is a particular sticking point.

Shareholder rights—or lack thereof—has long been an issue with Japan, particularly the far-too-ubiquitous scenario where corporations have piles of cash but pay peanuts in dividends. Year after year, the cash stockpile crushes profitability metrics such as return on equity (ROE) because the earned interest rate is in the basement.

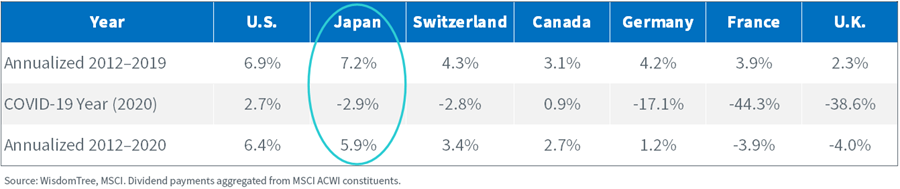

Nevertheless, sometimes the story does not completely line up with the actual situation on the ground. MSCI Japan’s component companies increased dividends at a 7% annual clip from 2012–2019. Perhaps more importantly, payouts were cut just 3% in reaction to COVID-19 lockdowns. That is a notably different experience than in most of the rest of the developed world (figure 1).

Figure 1: Dividend Growth, Developed Markets

Suddenly the market finds itself in a scenario where the MSCI Japan index—long notorious for paltry dividends—exceeds the yield of the S&P 500 by 71 basis points (2.03% vs. 1.32%). Our own WisdomTree Japan Hedged Equity Fund (DXJ) yields 2.82%, about double what can be found in the U.S. broad market.

Additionally, DXJ’s forward earnings multiple is 12.3, so its earnings yield is the reciprocal of that figure, 8.1%. In contrast, the S&P 500’s forward price-to-earnings (P/E) multiple is 22.2; its earnings yield is just 4.5%.

There are some promising developments for investors who itch for dividend boosts. With COVID-19 dominating global headlines, it was easy to miss the update to Japan’s corporate governance code, which happened in June.

Notable developments include a new requirement that the number of independent board directors must increase from two individuals to one-third of the mix. Additionally, on board diversity, there is a push to put non-Japanese in senior management, potentially mitigating cronyism. Another initiative that may help Japan’s stock market is a new requirement to publish disclosure materials in English.

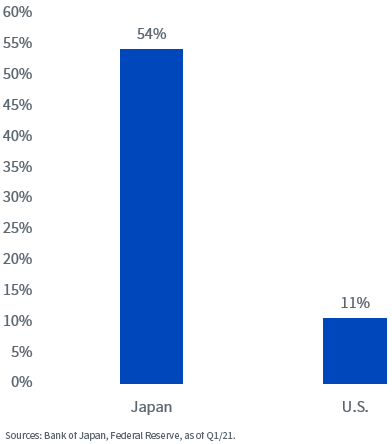

Something else to note: a common instinct to self-insure at the household level, which may help Japan’s economy hold up better than others in the event of some systemic shock. To wit, over half of household assets are held in bank accounts or cash, about five times the U.S. proportion (figure 2).

Figure 2: Household Cash & Deposits as Percentage of Total Assets

Things are clicking for Corporate Japan; with about 10 points of forward P/E “savings” in DXJ relative to the S&P 500, it could be a contrarian value play for investors willing to engage the world’s third-largest economy.

Beyond DXJ, two other mandates to investigate are the WisdomTree Japan SmallCap Dividend Fund (DFJ) and the WisdomTree Japan Hedged SmallCap Equity Fund (DXJS).

Unless otherwise stated, all data, as of 7/31/21, from WisdomTree Digital Portfolio Developer.

1 Source: Our World in Data.

2 Japan Reaches 100m COVID-19 Doses, Surpasses U.S. in Proportion of Older Folk Fully Vaccinated, Straits Times, 8/11/21.

Important Risks Related to this Article

Performance is historical and does not guarantee future results. Current performance may be lower or higher than quoted. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Standardized performance and 30-day SEC yield for DXJ is available here.

WisdomTree shares are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Total returns are calculated using the daily 4:00 p.m. net asset value (NAV). Market price returns reflect the midpoint of the bid/ask spread as of the close of trading on the exchange where Fund shares are listed. Market price returns do not represent the returns you would receive if you traded shares at other times.

This material must be preceded or accompanied by a prospectus. Please read the prospectus carefully before investing

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Funds focus their investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Investments in currency involve additional special risks, such as credit risk, interest rate fluctuations, derivative investments which can be volatile and may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As DXJ and DXJS can have a high concentration in some issuers, the Funds can be adversely impacted by changes affecting those issuers. Funds focusing their investments on certain sectors and/or smaller companies increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Due to the investment strategy of DXJ and DXJS, these Funds may make higher capital gain distributions than other ETFs. Please read each Fund’s prospectus for specific details regarding the Funds’ risk profiles.

Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

Share & Comment

Popular Posts

Categories

Related Links