So, You’re Interested in Artificial Intelligence…?

While artificial intelligence (AI) was always a “big topic”—and we could pick from various consultant research pieces to denote future predictions as to the impact on economic growth and productivity—talking about the gross domestic product (GDP) lacks that “sizzle” that gets people talking, messaging and sharing.

ChatGPT, on the other hand, with just that right balance between innovation, power and novelty, achieved virality. The immediate result is that more people are regularly discussing AI like it was any other normal topic at a veritable cocktail party.

Investors are re-engaging to better conceptualize the range of actions that they might consider if, in fact, they believe an AI exposure is appropriate within their specific portfolios.

Consideration 1: The GIANTS

In light of the recent concerns spurred on by perceptions of risk in the financial sector, some have noted that large companies associated with technology may be a relative “safe haven.” That doesn’t mean they will have positive returns—just that investors may be in search of significant cash balances and cash generation, and few companies do this better than Apple, Microsoft or Alphabet. And with all of the grief CEO Mark Zuckerberg has taken for his venture into the metaverse, few can even argue that, as a cash-generating business, Meta is still remarkable.

ChatGPT has brought large language models (LLMs) into focus, and certain longstanding rivalries between Microsoft and Alphabet have been brought to the forefront. Microsoft CEO Satya Nadella achieved a PR coup by getting certain publications to write about the possibility of a coming war in search.

Even if Microsoft’s PR announcements were not perfect, by any stretch, the world was quick to focus on perceived errors made by Google’s instantiation of its LLM, Bard. We’d be careful to remind readers that researchers at Google were responsible for developing the concept of the transformer (the “T” in GPT),1 and even if OpenAI2 has leaped ahead with the virality of its applications, Google does have some of the strongest AI research capabilities in the world. With its massive usage and the fact that Alphabet is also responsible for YouTube, sometimes Alphabet has to err toward caution as opposed to being able just to launch interesting AI technologies to its billions of users.

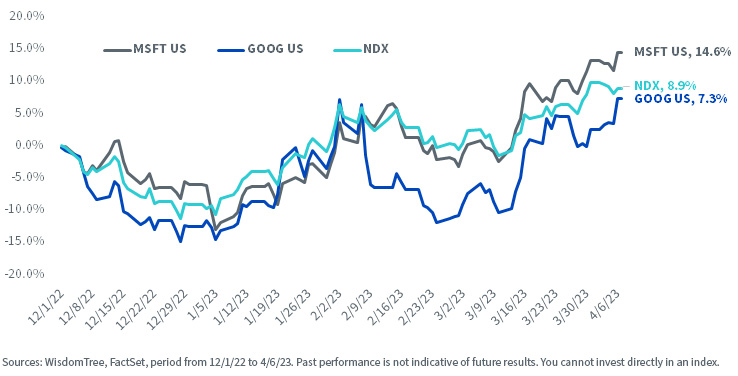

Figure 1: Performance of Microsoft (MSFT) and Alphabet (GOOG) Post ChatGPT Release (Shown along with Nasdaq 100 (NDX))

We simply pose one question: Over time, are they more likely to see their share prices moving on the basis of their perceived connection to AI, or are these large, diversified businesses susceptible to reflecting a bit on AI, a bit on the potential of different regulatory actions, a bit on their core legacy business interests…the list can go on?

Consideration 2: Processing Power

Nvidia has done an incredible job associating its offering with sheer processing power to facilitate the training and running of different large AI models. One sees this in the returns, in that one of the more important perceived areas of growth in semiconductors lies in providing the semiconductors that run data centers. Even if the inertia and current market share statistics indicate that Intel is a large player, the forward-looking prospects seem to favor other players.

AI does not require small amounts of incredibly accurate calculations—it requires very large amounts of calculations that converge toward accuracy due to their scale. The graphics processing unit (GPU) is equipped to do this better than the standard central processing unit (CPU) logic chip. Nvidia’s offering, therefore, went from being primarily for gamers—still a big market in itself—to gamers, data centers, companies exploring autonomous driving, basically, a truly endless list. Articles even cite a “Huang’s Law,” named after Nvidia founder and CEO Jensen Huang, which posits that the processing power of a GPU may more than double every two years.3

If we think of AI as an ecosystem, however, it’s important to recognize that semiconductors are also an ecosystem, in that Nvidia, by itself, could not necessarily bring physical semiconductors to the market. The way to think of it is that Nvidia is designing the chip, companies like Cadence4 and Synopsis are seeking to verify the feasibility of the designs and then a company like Taiwan

Semiconductor Manufacturing Co. (TSMC) is fabricating the chip. Each of these companies and different layers of the value chain—in this case, a very simplified view—may be trading in accordance with many different perceived risks, with share prices rising and falling in part due to expectations regarding the growth of AI and in part due to other factors.

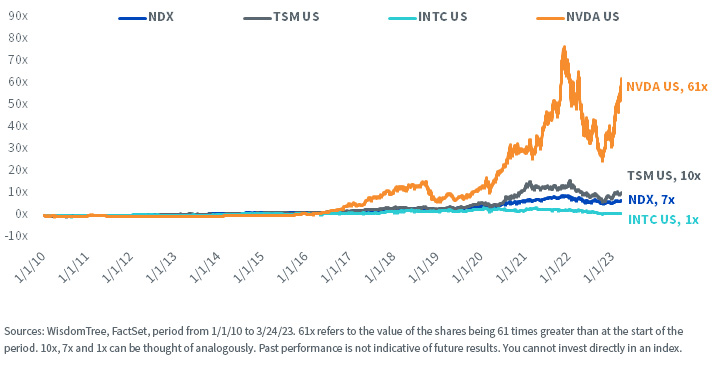

Figure 2: Performance of Nvidia (NVDA), Taiwan Semiconductor Manufacturing Co. (TSMC) and Intel (INTC) since 2010, Shown along with Nasdaq 100 Index (NDX)

Bottom Line on Processing Power: Semiconductors are very cyclical, in that demand tends to come in waves, and capital expenditures and investments seek to increase that capacity, leading to periods of undersupply and oversupply over time, with commensurate moves in the prices of the actual chips. And we have some of the bigger companies, like Alphabet, Tesla and Apple, seeking to design more and more of their own chips. This may favor a company like TSMC—the big players still need their chips to be fabricated—but may not favor other chip companies that seek to design chips.

Consideration 3: Diversified Value-Chain Approach

One of the principles we have espoused for some time is that AI has the potential to impact every industry, so it would not be appropriate to state that AI is solely this type of company and not that type of company. There are users of AI (think of TikTok, Netflix and YouTube), there are AI software providers (think of Nice, UiPath and even OpenAI), there are hardware players that allow AI to function (Nvidia, TSMC and Infineon) and there are some giant companies that when they make a small investment relative to their balance sheets, it could advance the space immeasurably (Microsoft, Amazon, Alphabet, Apple).

Picking individual winners is hard. Mixing the giants, the hardware providers and the software providers together can allow an overall strategy to be sensitive to different elements of the AI value chain getting hot and gaining attention at different points of a given economic cycle. It also helps to mitigate the risk of getting stuck in software when semiconductors are rallying or missing out on strong relative performance in the largest companies during market turmoil.

Finally, the nature of AI advances is not linear, in that we don’t know for sure from where or how they will come. One possible path forward from today could be Microsoft integrating the technology underlying GPT-4 across much of its Office 365 suite of programs, which would then mean billions would be using it virtually overnight.

The WisdomTree Artificial Intelligence and Innovation Fund (WTAI) was designed with the concept of a value chain or ecosystem-driven approach in mind. AI currently means many things and has the potential to influence many companies, and the strategy is designed to be focused on the megatrend but at the same time to recognize that the value may be captured by many different types of business models.

1 Source: Vaswani et al., “Attention is all you need,” 31st Conference on Neural Information Processing Systems (NIPS 2017), Long Beach, CA, USA.

2 As of March 30, 2023, OpenAI is not eligible for investment by public market investors.

3 Source: Christopher Mims, “Huang’s Law Is the New Moore’s Law and Explains Why Nvidia Wants ARM,” Wall Street Journal, 9/19/20.

4 As of March 30, 2023, Cadence had a weight of 2.05% in WTAI.

Important Risks Related to this Article

Click here for a full list of Fund holdings. Holdings are subject to change.

There are risks associated with investing, including the possible loss of principal. The Fund invests in companies primarily involved in the investment theme of artificial intelligence (AI) and innovation. Companies engaged in AI typically face intense competition and potentially rapid product obsolescence. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Additionally, AI companies typically invest significant amounts of spending in research and development, and there is no guarantee that the products or services produced by these companies will be successful. Companies that are capitalizing on innovation and developing technologies to displace older technologies or create new markets may not be successful. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is governed by an Index Committee, and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Share & Comment

Popular Posts

Categories

Related Links

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Blake Heimann is a Senior Associate on the Quantitative Research & Multi Asset Solutions team at WisdomTree, based in Europe. He initially joined WisdomTree in 2020 as an Analyst on the Research team in the U.S. In his current role, he is responsible for supporting the creation, maintenance, and reconstitution of equity and digital asset indices.

Blake's finance career began in 2017 at TD Ameritrade, where he started as an Analyst before transitioning to a role as a Quantitative Analyst. During this time, he focused on research and development of machine learning applications in finance. Blake holds bachelor's degrees in Mathematics and Economics from Iowa State University, and he has completed his Master's in Computer Science with a specialization in Machine Learning at Georgia Tech.