DDWM

Dynamic International Equity Fund

Published May 15, 2026

Global Head of Research

On January 7, 2026, the WisdomTree Dynamic International Equity Fund (DDWM) crossed its 10-year anniversary. That milestone matters, but the more important point for investors today is not simply that the strategy has been around for a decade. It is that DDWM has now shown how a disciplined developed international equity process can perform across very different environments:

In that sense, DDWM's record is less a story about longevity for its own sake and more a record of how a repeatable process behaved when markets repeatedly changed the rules.

That matters even more because the case for developed international equities no longer rests on a purely theoretical diversification argument. Broad non-U.S. developed markets have recently delivered meaningful absolute returns, while still offering characteristics many U.S. investors say they want more of:1

DDWM approaches this opportunity through dividend-paying companies across developed markets outside the U.S.

DDWM is also built with a second layer of discipline that is easy to overlook but important in practice: a dynamic currency hedge. For U.S.-based investors, international equity returns are never just about stock selection. They are also shaped by the path of the U.S. dollar relative to the euro, yen, pound and other developed market currencies. Rather than making a static all-or-nothing call, DDWM has the flexibility to raise or lower its hedge based on changing market conditions. In some periods that can help reduce currency-related volatility. In others, it can help preserve the benefit of a favorable carry backdrop or a weakening dollar. Everyone can see currencies moving; far fewer investors have a clear framework for what to do about them. DDWM offers one systematic answer.

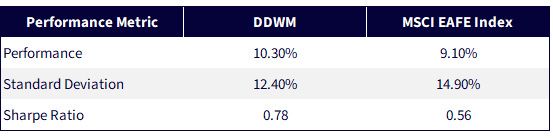

As of January 27, 2026, DDWM delivered annualized total returns of 10.73%, versus 9.66% for the MSCI EAFE Index. We believe that gap is meaningful, particularly because it was earned over a full market cycle rather than a short tactical window.

Digging further into the return profile, the dynamic currency hedge was an important contributor over much of the period. For extended stretches of the past decade, U.S. short-term rates were above those in many developed international markets. In that environment, hedging foreign currency exposure could contribute positively even before considering the direction of the currencies themselves. That feature does not guarantee future outperformance, but it does highlight that currency management has been a material part of DDWM's overall result rather than a side detail.

Figure 1b: Standardized Returns

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of April 25, 2026, but showing returns for the period ended April 24, 2026 for Figure 1a Performance and March 31, 2026 for the standard deviation and Sharpe ratio, as well as for Figure 1b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

The broader market backdrop also makes this discussion timely. After many years in which U.S. equities dominated global leadership, developed international markets have started to remind investors why geographic diversification still matters.

Non-U.S. equities snapped back in 2025, and the MSCI EAFE Index returned more than 31%. Then, looking at year-to-date 2026 through April 24th, we see that the MSCI EAFE Index is still keeping pace with an S&P 500 Index that started off dramatically trailing, but that has also rallied back of late.2 In other words, U.S. investors no longer need to frame developed international exposure as merely a contrarian bet on mean reversion. They can frame it as exposure to a part of the market that has recently delivered strong performance while still looking fundamentally differentiated from the U.S.-led benchmark mix.

As DDWM enters its second decade, the takeaway is not simply that it survived a difficult period for international investing. It is that developed international equities remain relevant for U.S. portfolios, and that the right implementation still matters. For investors who want exposure beyond the United States, but who also care about income, valuation discipline and a more thoughtful approach to currency risk, DDWM represents an interesting way to get there. The point is not to replace U.S. equities. It is to remember that strong portfolio construction rarely comes from looking in only one place.

Source: MSCI Inc. (2026, March 31). MSCI EAFE Index (USD): Index factsheet. MSCI.

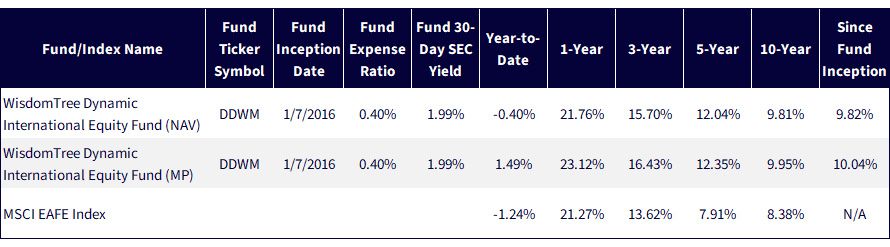

Sources: WisdomTree, Morningstar and Factset, with data accessed from WisdomTree’s Fund Compare tool with the broader PATH Suite of tools. Data was accessed as of April 26, 2026. Past performance is not indicative of future results.

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund invests in derivatives in seeking to obtain a dynamic currency hedge exposure. Derivative investments can be volatile, and these investments may be less liquid than other securities, and more sensitive to the effects of varied economic conditions. Derivatives used by the Fund may not perform as intended. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Dynamic International Equity Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.