DDWM

Dynamic International Equity Fund

Published June 5, 2025

Global Head of Research

Something subtle but significant is underway in global equity markets. After years of U.S.-centric asset allocation dominance, 2025 is shaping up as a pivot point. Inflows into equity strategies that deliberately exclude U.S. exposure have reversed a multiyear trend of net outflows, with more than $2.5 billion added in just the last three months.1 This is not simply a temporary reaction to political volatility; it's an early recognition that the rest of the world is increasingly writing its own macroeconomic and corporate profitability stories. And for U.S.-based investors, the implications are timely: diversification is no longer a hedge—it may be a source of structural return.

European equities have outperformed consensus expectations in 2025, and not just because of currency dynamics.2 Core sectors like banking and defense have benefited from a steepening yield curve, a surge in defense commitments and recovering earnings power. While gross domestic product (GDP) growth remains subdued, equity markets are reflecting something deeper: stock-level dispersion is unusually high, signaling a return to idiosyncratic alpha. Structurally, five forces are at play:

3

In valuation terms, European equities continue to trade at a meaningful discount to U.S. peers—yet the earnings base is strengthening beneath the surface.

In Japan, what had been a hopeful reform story is increasingly showing up in the numbers. Domestic-oriented companies have outperformed exporters, bolstered by wage growth, better governance and targeted capital allocation improvements.4 While global investors have long debated the sustainability of Japan’s equity rallies, the current environment is different. The Tokyo Stock Exchange’s push for governance reform, combined with pressure to unwind legacy cross-holdings and simplify parent-subsidiary structures, is translating into better margin profiles and return on equity.

5 Strategists see the potential for continued rerating as Japanese companies deliver earnings less sensitive to the yen and more tied to corporate behavior.

The rethink of geographic allocation is not simply about avoiding risks—it’s about capturing evolving structural asymmetries. While U.S. equities remain powerful innovation engines, their dominance in global indexes now masks the opportunity set elsewhere. Many institutional equity portfolios carry a hidden overexposure to U.S. mega-cap tech, and the question is not whether to abandon it, but whether the next decade’s return profile will be better balanced with regions undergoing deep structural change.6 Europe and Japan are offering what U.S. equities delivered in past cycles: rerating potential linked to margin expansion, not just revenue growth.

Perhaps most compelling is that beneath modest top-down GDP figures, international markets are offering highly fertile ground for active strategies. Stock-level dispersion in Europe is running above historical averages, and factors like idiosyncratic momentum, earnings revisions and accruals are delivering higher-than-normal Sharpe ratios. These are precisely the environments where stock selection—not sector or beta allocation—adds real value.7 For U.S.-based allocators, this is not about abandoning what has worked domestically but recognizing that the alpha is no longer confined by geography. The structural bull cases being built abroad—especially in sectors like energy infrastructure, financial modernization and dual-use technology—are too material to ignore.

The WisdomTree Dynamic International Equity Fund (DDWM)

DDWM is designed to track the total return performance, before fees and expenses, of the WisdomTree Dynamic International Equity Index. This broad approach (2,439 positions as of May 23, 2025) includes developed international dividend payers and weights them based on their cash dividends. Weighting in this way as opposed to market capitalization tends to mitigate the risk of undue exposure to firms with higher valuations.

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 5/21/25, with returns as of 3/31/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Prior to April 30, 2025, the Fund was known as the WisdomTree Dynamic Currency Hedged International Equity Fund. Past performance is not indicative of future results. Investment returns and the principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

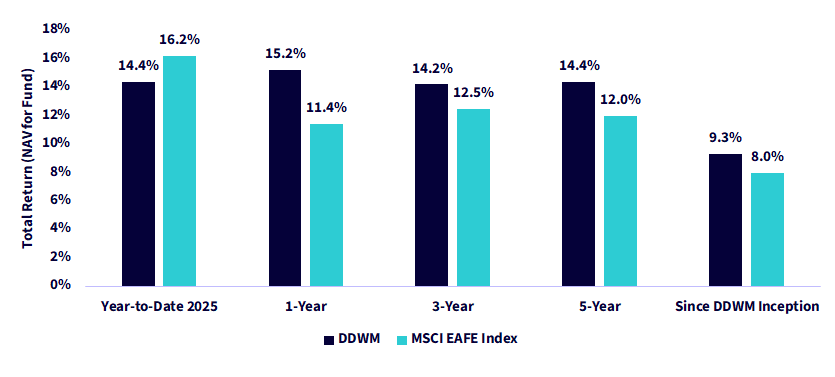

Figure 2 highlights the consistent outperformance of the DDWM strategy over the MSCI EAFE Index across multiple timeframes, particularly over the past one, three and five years. While the MSCI EAFE leads year-to-date in 2025, DDWM has delivered higher compounded returns over the longer term, including since inception. This pattern points to a strategy that rewards patience and has the potential to compound effectively across cycles.

Figure 2: DDWM’s Long-Term Return Strength vs. MSCI EAFE Index

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 5/21/25, with returns as of 5/20/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Prior to April 30, 2025, the Fund was known as the WisdomTree Dynamic Currency Hedged International Equity Fund. Past performance is not indicative of future results. Investment returns and the principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

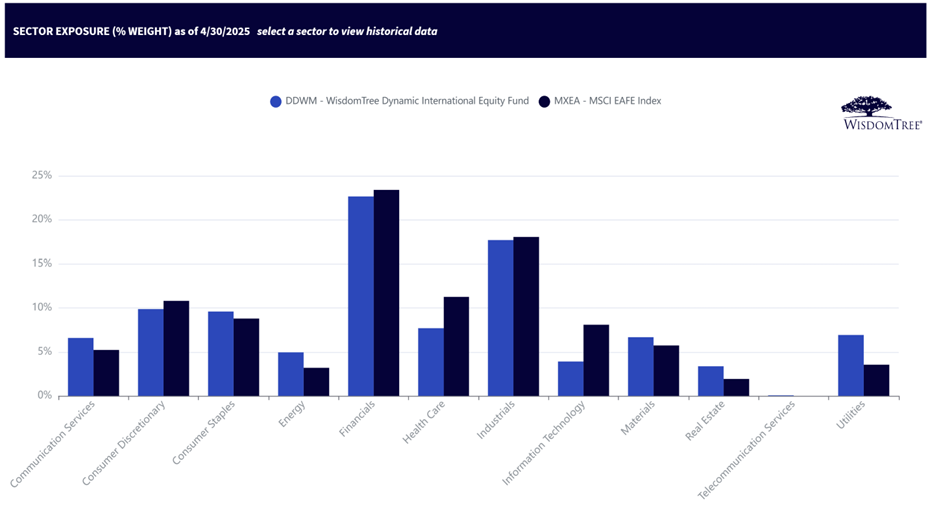

Figure 3 compares sector allocations between DDWM and the MSCI EAFE Index as of April 30, 2025. DDWM exhibits notable over-weight positions in Financials, Health Care and Utilities while under-weighting sectors like Information Technology and Real Estate compared to the benchmark. The allocation suggests an emphasis on quality and defensiveness, with a tilt toward income-generating and stable-growth sectors.

Figure 3: DDWM’s Sector Dispersion Is Not Extreme Compared to MSCI EAFE Index

Sources: WisdomTree, FactSet. Subject to change.

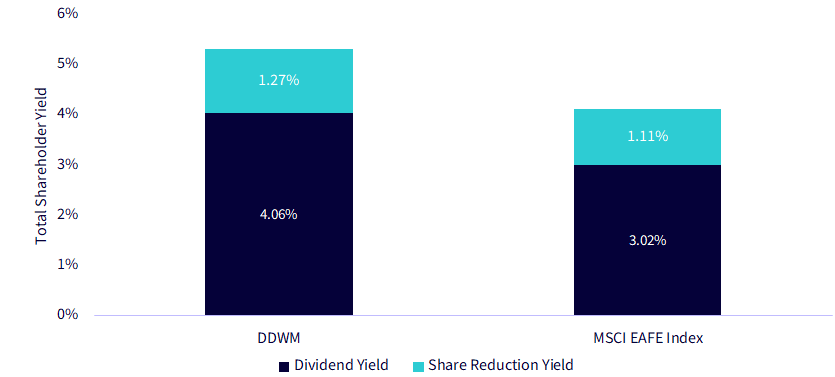

Figure 4 highlights that DDWM delivers a higher total shareholder yield than the MSCI EAFE Index, driven by both dividend yield and share reduction yield. By weighting holdings based on cash dividends, DDWM naturally emphasizes companies with stronger income distribution practices, resulting in a 4.06% trailing 12-month dividend yield versus 3.02% for the benchmark. While share repurchases are not the primary selection factor, the portfolio still benefits from a higher 1.27% share reduction yield.

Sources: WisdomTree, FactSet. Data as of 4/30/25. Subject to change. Past performance is not indicative of future results. Investment returns and the principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

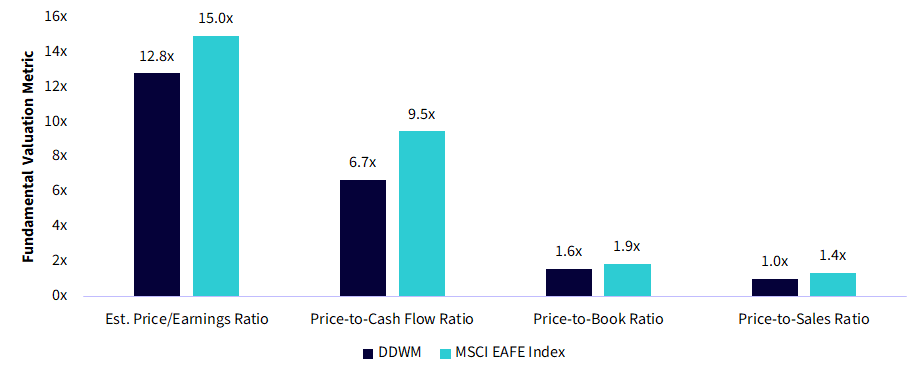

Figure 5 underscores DDWM’s relative valuation advantage across key metrics compared to the MSCI EAFE Index. Whether looking at price-to-earnings, price-to-cash flow or price-to-book, DDWM consistently trades at more attractive levels—helping mitigate valuation risk. For investors concerned about elevated multiples in U.S. markets, this signals a disciplined approach to international equity exposure with a strong value orientation.

Figure 5: DDWM’s Overall Lower Valuation vs. MSCI EAFE Index

Sources: WisdomTree, FactSet. Data as of 4/30/25. Subject to change.

In a world where investors are increasingly questioning concentration risk and valuation extremes in U.S. equities, DDWM presents a differentiated, rules-based approach to international markets that blends quality, income and valuation discipline. Its emphasis on dynamic currency hedging, shareholder yield and lower valuation multiples delivers a portfolio designed to navigate global complexity without overpaying for growth. For those seeking to rebalance their equity exposure toward regions undergoing meaningful structural reform—while still demanding disciplined capital return and resilient fundamentals—DDWM stands out as a compelling vehicle to reengage with the broader opportunity set beyond U.S. borders.

1Source: “Investors flock to equity funds that exclude US,” Financial Times, 5/13/25.

2Source: “Europe Insight: European equities mid-year outlook – Navigating choppy waters,” Morgan Stanley, Morgan Stanley Research, 5/21/25.

3Source: Morgan Stanley, 2025.

4Source: “Japan Insight: Japan equity strategy mid-year outlook – Patience before triumph,” Morgan Stanley MUFG, Morgan Stanley Research, 5/20/25.

5Source: Morgan Stanley MUFG, 2025.

6Source: Morgan Stanley, 2025.

7Source: Morgan Stanley, 2025.

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund invests in derivatives in seeking to obtain a dynamic currency hedge exposure. Derivative investments can be volatile, and these investments may be less liquid than other securities, and more sensitive to the effects of varied economic conditions. Derivatives used by the Fund may not perform as intended. A Fund that has exposure to one or more sectors may be more vulnerable to any single economic or regulatory development. This may result in greater share price volatility. The composition of the Index underlying the Fund is heavily dependent on quantitative models and data from one or more third parties, and the Index may not perform as intended. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Prior to April 30, 2025, the Fund was known as the WisdomTree Dynamic Currency Hedged International Equity Fund. The Fund’s ticker, investment objective and principal investment strategy remain unchanged.

Dynamic International Equity Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.