Don’t Mistake Speculation for Strength: The Mirage of Small-Cap “Junk” Outperformance

Published January 9, 2026

Christopher Gannatti, CFA

Global Head of Research

Brian Manby, CFA

Associate, Investment Strategy

Key Takeaways

- In 2025, speculative small-cap stocks with no earnings or dividends have sharply outperformed quality peers, driven by a surge in risk appetite and retail investor flows.

- Despite short-term momentum, valuation gaps between high- and low-quality small caps have widened significantly, creating a potential setup for mean reversion.

- Investors seeking to capitalize on a shift back to fundamentals may consider the WisdomTree U.S. SmallCap Quality Dividend Growth Fund (DGRS), which offers higher-quality metrics at discounted valuations relative to broader benchmarks like IWM.

U.S. small-cap equities have defied traditional logic in 2025. The companies investors have typically prized for their prudence, those with steady earnings and consistent dividends, have lagged behind the more speculative corners of the market. Instead, firms with no profits and no payouts have been leading performance charts, marking a striking reversal of the patterns that dominated much of the post-global financial crisis era.

- Risk Appetite Revival: Speculative small caps are benefiting from renewed enthusiasm for growth optionality rather than cash flow discipline.

- Liquidity and Leverage Effects: Easy financial conditions and the return of retail flows have amplified momentum in unprofitable names.1

- Valuation Divergence: Dividend payers and profitable small-cap firms now trade at unusually wide valuation discounts, potentially setting up a mean-reversion opportunity.

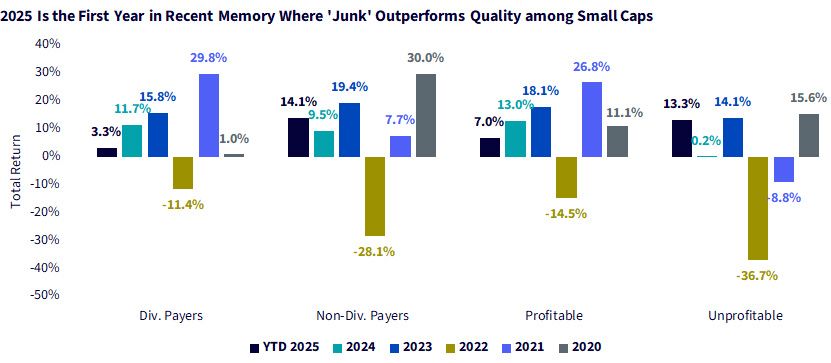

Figure 1 captures a rare market inversion: In 2025, unprofitable and non-dividend-paying small caps are sharply outperforming their higher-quality peers. After years when fundamentals drove returns, investor sentiment has pivoted toward speculative growth. The data underscores a risk-on rotation, liquidity-driven exuberance and a potential setup for future mean reversion.

Figure 1: Something New under the Sun?

Sources: WisdomTree, MSCI, FactSet, as of 11/3/25. Past performance is not indicative of future results. You cannot invest directly in an index. Profitable (unprofitable) small caps are defined as constituents of the MSCI USA Small Cap Index that had positive (negative) trailing 12-month earnings as of the most recent calendar year-end. Returns represent the weighted average year-to-date and calendar year returns among constituents using index weights as of the beginning of the return period. Annualized returns are calculated based upon calendar year and year-to-date 2025 returns, which individually use beginning-of-evaluation period weights.

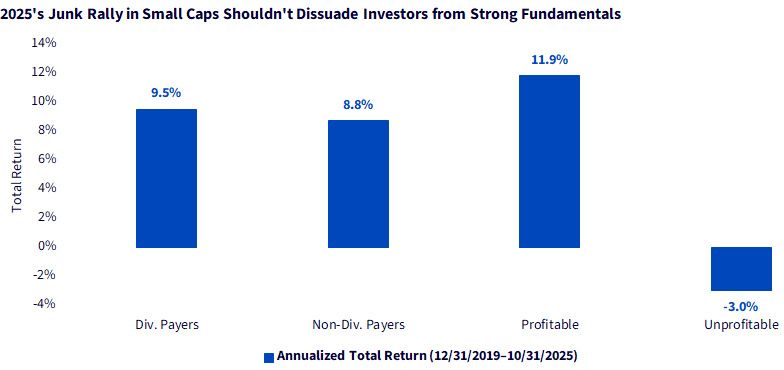

Despite 2025's surge in "junk" small caps, longer-term results, shown in figure 2, reaffirm the value of fundamentals. Over the past six years, profitable and dividend-paying companies have delivered the strongest compounded gains, while unprofitable firms remain in negative territory. The data highlights that short-term speculation fades, but quality compounds over time.

Figure 2: Longer Horizons May Look Different from Shorter Periods in Small-Cap Performance

Sources: WisdomTree, MSCI, FactSet, as of 11/3/25. Past performance is not indicative of future results. You cannot invest directly in an index. Profitable (unprofitable) small caps are defined as constituents of the MSCI USA Small Cap Index that had positive (negative) trailing 12-month earnings as of the most recent calendar year-end. Returns represent the weighted average year-to-date and calendar year returns among constituents using index weights as of the beginning of the return period. Annualized returns are calculated based upon calendar year and year-to-date 2025 returns, which individually use beginning-of-evaluation period weights.

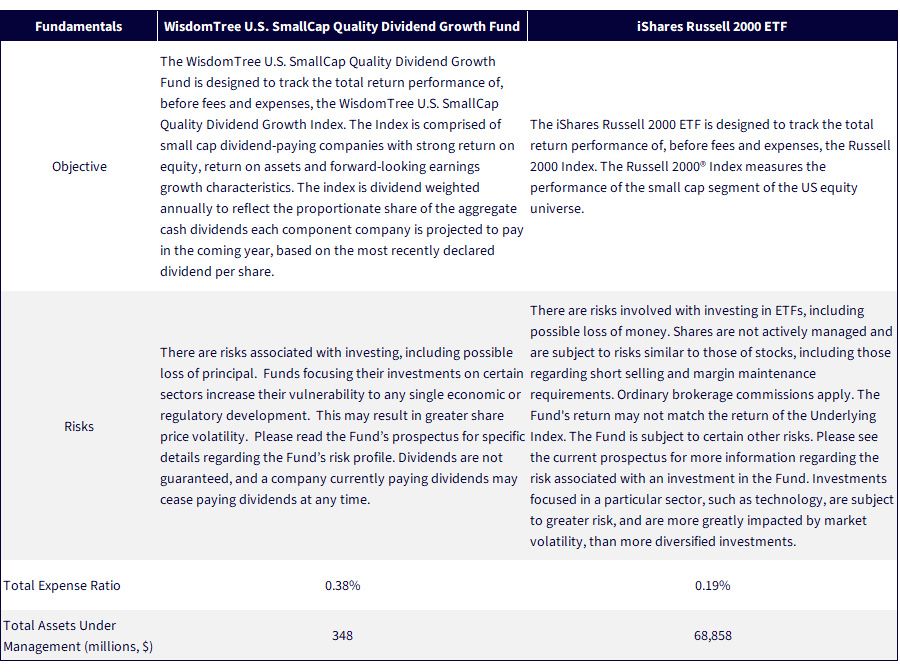

Conclusion: A Look at Two Exchange-Traded Funds Focused on U.S. Small Caps

The most widely referenced benchmark for U.S. small-cap equity performance is the Russell 2000 Index. The iShares Russell 2000 ETF (IWM) is designed to track the total return performance, before fees, of this benchmark. As of September 30, 2025, it had roughly 28% of its weight in companies that had negative earnings over the prior 12 months.2

The WisdomTree U.S. SmallCap Quality Dividend Growth Fund (DGRS) is designed to track the total return performance of an index focused on higher-quality small-cap companies that all pay dividends.3 They also have relatively higher return on equity and return on assets measures.

Therefore, we can look at:

- IWM as a broad-market benchmark with significant exposure to more speculative small-cap stocks.

- DGRS as a more focused strategy on U.S. small caps that emphasizes the higher-quality angle.

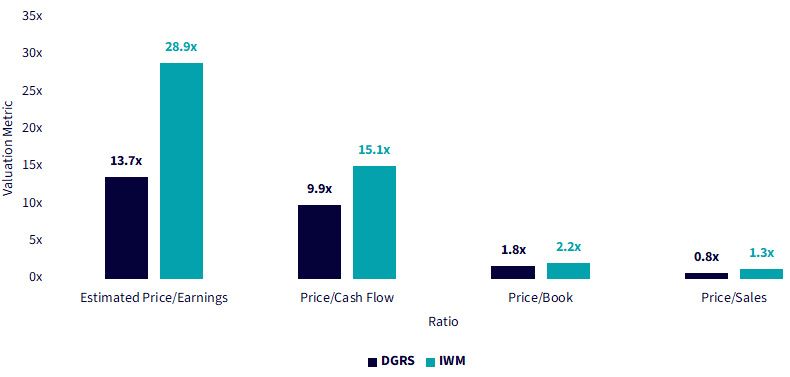

For those investors considering that the speculative rally may end, we wanted to focus on two of the following figures. Figure 3a indicates the valuation discount, on multiple metrics, of DGRS relative to IWM.

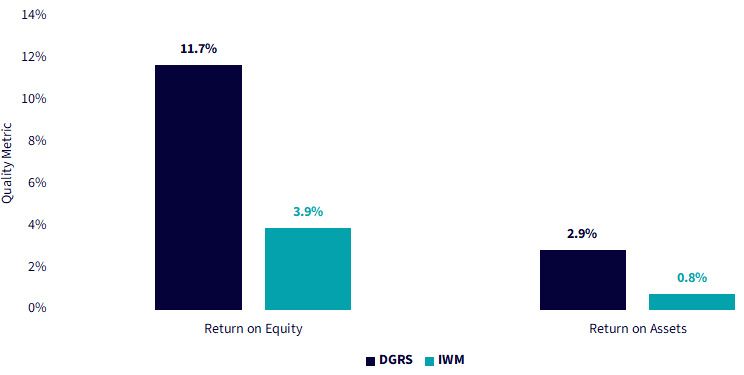

Figure 3b indicates the return on equity and return on assets of DGRS versus IWM.

Figure 3a: DGRS Shows a Valuation Discount on Multiple Measures against IWM

Sources: WisdomTree, FactSet, Morningstar, with data as of 9/30/25.

Figure 3b: DGRS Shows Significantly Higher Quality Metrics than IWM

Sources: WisdomTree, FactSet, Morningstar, with data as of 9/30/25

If the trend shifts back to rewarding higher-quality small caps, we think that DGRS may be particularly well positioned.

Figure 4: Additional Information

Sources: Specific Fund pages on the WisdomTree and iShares website, with AUM figures as of 11/5/25.

1 Source: "Small-cap stocks gain momentum: A new era of retail-driven growth and earnings optimism," AInvest, 10/25/25.

2 Sources: WisdomTree, FactSet, Morningstar, with data accessed as of 11/6/25 within WisdomTree's Fund Comparison tool.

3 This index is the WisdomTree U.S. SmallCap Quality Dividend Growth Index.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Funds focusing their investments on certain sectors and/or smaller companies increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

About the contributors

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Brian Manby, CFA

Associate, Investment Strategy

Brian Manby joined WisdomTree in October 2018 as an Investment Strategy Analyst. He is responsible for assisting in the creation and analysis of WisdomTree’s model portfolios, as well as helping support the firm’s research efforts. Prior to joining WisdomTree, he worked for FactSet Research Systems, Inc. as a Senior Consultant, where he assisted clients in the creation, maintenance and support of FactSet products in the investment management workflow. Brian received a B.A. as a dual major in Economics and Political Science from the University of Connecticut in 2016. He is holder of the Chartered Financial Analyst designation.