GDE

Efficient Gold Plus Equity Strategy Fund

Published July 29, 2025

Global Head of Research

Gold's renewed prominence in 2025 has reignited an age-old portfolio debate: how much room, if any, should the yellow metal occupy in a long-term asset allocation?

On the surface, the appeal is clear. Amid rising concerns about the U.S. fiscal trajectory, investors are taking a fresh look at gold's potential role as a hedge—not against imminent disaster, but against a slow-burn erosion of the dollar's purchasing power over time. In a world where fiscal dominance may gradually supplant monetary orthodoxy, this marks a meaningful shift. And to be fair, gold has already delivered strong returns through the first five months of 2025,1 further strengthening its near-term narrative.

But investors must navigate this moment with discipline. For all its tactical luster, gold remains structurally constrained: it generates no income, pays no dividend and compounds nothing. Its enduring value lies in preserving purchasing power and offering convexity during periods of monetary debasement, inflation shocks or geopolitical instability. These are real benefits—but they come at a price.

Allocating to gold isn't free. The core problem isn't gold's lack of productivity—it's what must be displaced to hold it. In most portfolios, that means reducing exposure to equities, the highest real-returning asset class in recorded history.

Professor Jeremy Siegel's seminal research puts equity returns at roughly 6.8% real annually over two centuries.2 That compounding engine, driven by reinvested earnings and global innovation, is unrivaled. While no asset class dominates in all environments, equities remain the centerpiece for any investor with a multi-decade horizon. From this vantage, the act of shifting capital from equities to gold is less about diversifying and more about truncating long-term upside.

This isn't a dismissal of gold. It's a call for clarity about trade-offs.

Traditionally, the answer has been no—allocating to gold required selling something else, usually equities. But modern portfolio construction offers new tools that render this trade-off less binary. Enter capital-efficient strategies.

Most investors looking at gold's sharp run-up in the first half of 2025 face a classic dilemma: the fear of missing out collides with the fear of being late. Emotionally, it feels like the trade has already worked—allocating now risks chasing past performance. Rationally, they understand that reallocating to gold often means taking capital from equities or other high-potential assets. This amplifies the potential for regret: if gold stalls or reverses, the investor not only misses upside elsewhere but did so in pursuit of what already happened. However, capital-efficient strategies offer a way out of this corner. By maintaining core exposures—particularly to equities—while layering in gold exposure synthetically or structurally, investors can participate in potential continued gold upside without making a stark either/or decision. This reduces the emotional and financial burden of timing decisions and reframes the allocation not as a binary bet, but as an additive, regret-minimizing enhancement.

WisdomTree's capital-efficient ETFs are engineered to deliver equity participation while creating room for diversifiers, all within a single line item of a portfolio. For investors concerned about the opportunity cost of de-equitizing, this could be a game changer.

We thought it could be useful to explore how an allocation to gold could impact a portfolio of U.S. assets, starting at 60% equities and 40% fixed income.

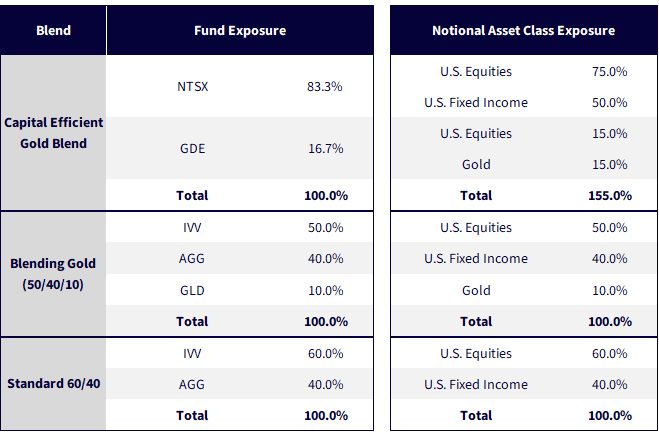

Looking at figure 1, we can see that Blending Gold (50/40/10) is taking the traditional approach. GLD at 10% represents one-fifth the relative exposure to U.S. equities, with IVV at 50%.

Within Capital Efficient Gold Blend, we are using two capital-efficient ETF allocation tools. An 83.3% allocation to NTSX leads us to a U.S. equity starting point of 75%. If we then allocate 16.7% to GDE, we get a 15% overall gold exposure (15% is one-fifth of the 75%).

But Capital Efficient Gold Blend does not stop there. GDE also generates 15% exposure to U.S. equities, bringing the total U.S. equity exposure to 90%. If one had placed 100% of the allocation into NTSX, by design, this would also generate 90% exposure to U.S. equities. Therefore, it is like we added GDE and did not take anything away from U.S. equities. Of course, capital-efficient exposure is not a free lunch, in the sense that using leverage in this way can increase volatility. To think about risk, the worst case would be if U.S. equities, U.S. fixed income and gold are all going down during the same time frame. Historical analysis indicates that this has not happened often on a calendar year basis, but 2022 would be the most recent such year.

Source: WisdomTree.

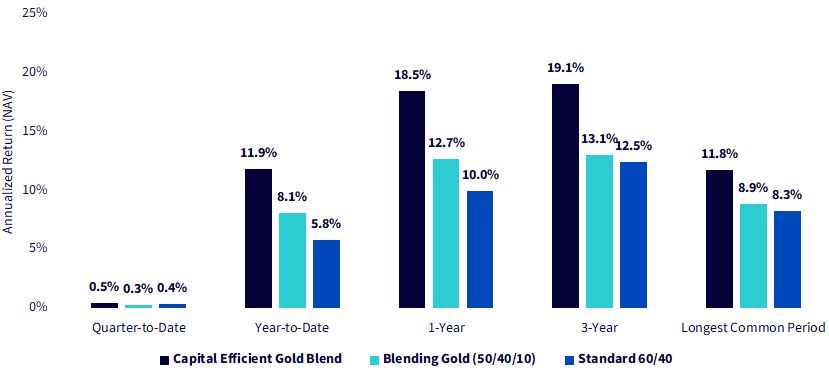

Figure 2 shows the standardized period returns of the different blends as well as the different ETFs that are used to create them. This data is as of June 30, 2025.

Sources: WisdomTree, FactSet, Morningstar, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 7/12/25, with returns as of 6/30/25. NAV denotes total return performance at net asset value. MP denotes market price performance. The performance data quoted represents past performance and is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: NTSX, GDE, IVV, AGG, GLD.

The first five months of 2025 will not be remembered for a smooth, upward trending path of U.S. equity performance.

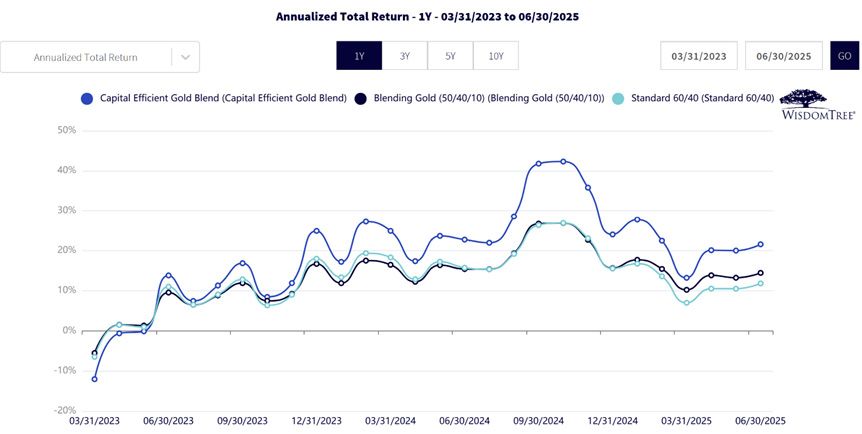

The speed of these shifts left many feeling a bit of whiplash when looking at their portfolios. We can see in figure 3 how well the different aforementioned blends have done over some of these periods.

Sources: WisdomTree, FactSet, Morningstar, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 7/12/25, with returns as of 7/11/15. The longest common period is from the inception of GDE, March 17, 2022. NAV denotes total return performance at net asset value. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker:NTSX, GDE, IVV, AGG, GLD.

When we pulled up the rolling 12-month periods (limited due to GDE having just over three years of total live history), we saw something surprising.

Sources: WisdomTree, FactSet, Morningstar, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 7/12/25, with returns as of 6/30/25. NAV denotes total return performance at net asset value. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker:NTSX, GDE, IVV, AGG, GLD. For fund prospectus, click the relevant ticker: NTSX, GDE, IVV, AGG, GLD.

At its core, the debate about gold versus equities is a test of how investors think about time, risk and opportunity. Gold shines when fear dominates, but equities build enduring wealth when patience prevails—a truth reinforced across centuries of market history and crisply articulated in Stocks for the Long Run. The real risk with gold isn't that it fails; it's that by funding it through reduced equity exposure, investors may quietly surrender the engine of real compounding. Yet today's portfolio tools, like WisdomTree's capital-efficient strategies, offer a more sophisticated way forward: a chance to embrace the tactical advantages of gold without abandoning the structural advantages of stocks. In a market defined by new threats and new technologies, the smartest investors aren't making blunt trade-offs—they're finding ways to stack advantages. The future belongs to those who can hedge wisely without giving up their claim on growth.

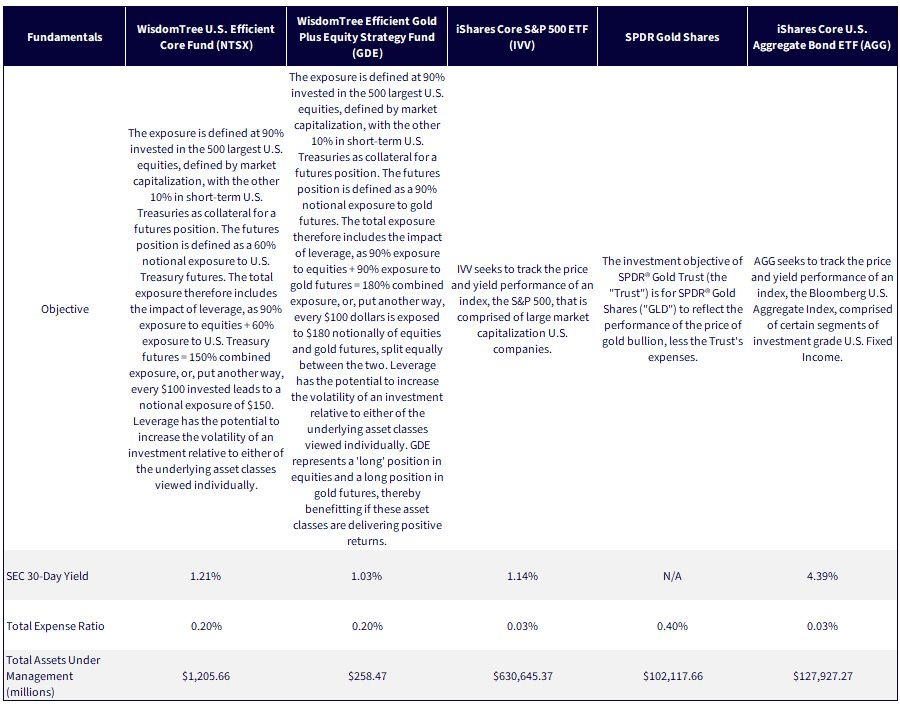

Sources: WisdomTree and individual fund sponsor websites for the assets under management, current as of 7/11/25. SEC 30-Day Yield as of 6/30/25.All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund. For fund prospectus, click the relevant ticker: NTSX, GDE, IVV, AGG, GLD.

There are risks associated with investing, including the possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

GDE: The Fund is actively managed and invests in U.S.-listed gold futures and U.S. equity securities. The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. U.S. equity securities, such as common stocks, are subject to market, economic and business risks that may cause their prices to fluctuate. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains.

NTSX: While the Fund is actively managed, the Fund’s investment process is expected to be heavily dependent on quantitative models and the models may not perform as intended. Equity securities, such as common stocks, are subject to market, economic and business risks that may cause their prices to fluctuate. The Fund invests in derivatives to gain exposure to U.S. Treasuries. The return on a derivative instrument may not correlate with the return of its underlying reference asset. The Fund’s use of derivatives will give rise to leverage and derivatives can be volatile and may be less liquid than other securities. As a result, the value of an investment in the Fund may change quickly and without warning and you may lose money. Interest rate risk is the risk that fixed income securities, and financial instruments related to fixed income securities, will decline in value because of an increase in interest rates and changes to other factors, such as perception of an issuer’s creditworthiness.

IVV: Carefully consider the Fund’s investment objectives, risk factors and charges and expenses before investing. This and other information can be found in the Fund’s prospectus, and, if available, summary prospectus, which may be obtained by calling 1-800-iShares (1-800-474-2737) or by visiting www.iShares.com or www.blackrock.com. Read the prospectus carefully before investing. Investing involves risk, including the possible loss of principal.Diversification may not protect against market risk or loss of principal. Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Any applicable brokerage commissions will reduce returns. The iShares Funds are not sponsored, endorsed, issued, sold or promoted by S&P Dow Jones Indices LLC, nor does this company make any representation regarding the advisability of investing in the Funds. BlackRock is not affiliated with S&P Dow Jones Indices LLC. BlackRock provides compensation in connection with obtaining or using third-party ratings and rankings. © 2025 BlackRock, Inc. or its affiliates. All rights reserved. iSHARES, iBONDS and BLACKROCK are trademarks of BlackRock, Inc., or its affiliates. All other trademarks are those of their respective owners. FOR MORE INFORMATION, VISIT WWW.ISHARES.COM OR CALL 1-800 ISHARES (1-800-474-2737).

AGG: Carefully consider the Fund’s investment objectives, risk factors and charges and expenses before investing. This and other information can be found in the Fund’s prospectus and, if available, summary prospectus, which may be obtained by calling 1-800-iShares (1-800-474-2737) or by visiting www.iShares.com or www.blackrock.com. Read the prospectus carefully before investing. Investing involves risk, including the possible loss of principal. Fixed income risks include interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Diversification may not protect against market risk or loss of principal. Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Any applicable brokerage commissions will reduce returns. The iShares Funds are distributed by BlackRock Investments, LLC (together with its affiliates, “BlackRock”). The iShares Funds are not sponsored, endorsed, issued, sold or promoted by Bloomberg, nor does this company make any representation regarding the advisability of investing in the Funds. BlackRock is not affiliated with Bloomberg. BlackRock provides compensation in connection with obtaining or using third-party ratings and rankings. © 2025 BlackRock, Inc. or its affiliates. All rights reserved. iSHARES, iBONDS and BLACKROCK are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners. FOR MORE INFORMATION, VISIT WWW.ISHARES.COM OR CALL 1-800 ISHARES (1-800-474-2737).

GLD: Investing involves risk, and you could lose money on an investment in SPDR® Gold Trust (“GLD® ” or “GLD”). ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns. Commodities and commodity-index-linked securities may be affected by changes in overall market movements, changes in interest rates and other factors such as weather, disease, embargoes, or political and regulatory developments, as well as trading activity of speculators and arbitrageurs in the underlying commodities. Frequent trading of ETFs could significantly increase commissions and other costs such that they may offset any savings from low fees or costs. Diversification does not ensure a profit or guarantee against loss. There can be no assurance that a liquid market will be maintained for ETF shares. Investing in commodities entails significant risk and is not appropriate for all investors. Important Information Relating to GLD: GLD has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents GLD has filed with the SEC for more complete information about GLD and this offering. Please see the GLD prospectus for a detailed discussion of the risks of investing in GLD shares. When distributed electronically, the GLD prospectus is available by clicking here. You may get these documents for free by visiting EDGAR on the SEC website at sec.gov or by visiting spdrgoldshares.com. Alternatively, GLD or any authorized participant will arrange to send you the prospectus if you request it by calling 866.320.4053.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.