EPI

India Earnings Fund

Published February 12, 2026

Global Head of Research

Macro Strategist, Model Portfolios

Director, Quantitative Research

The announcement of a U.S.–India trade agreement has quickly re-entered global market conversations, and with good reason. For investors who have watched India oscillate between optimism and frustration over the past year, the announcement feels like a release of pressure. Tariff uncertainty is easing, geopolitical alignment is becoming clearer, and markets have responded accordingly.

But trade deals rarely deliver their value all at once. For India, the real significance lies not in the immediate headlines, but in what this agreement represents: a key step along a longer path toward policy clarity, strategic relevance and durable economic growth.

Why the Trade Deal Matters, And Why It's Not Enough on Its Own

Reports suggest the U.S. and India have agreed to move toward a reciprocal tariff rate of roughly 18%, a sharp improvement from the punitive levels briefly imposed in 2025 and one that places India favorably relative to other Asian emerging markets. The U.S. is India's largest trading partner, accounting for close to 20% of goods exports, and the removal of trade-related uncertainty has immediate implications for business confidence and external demand.1

Markets tend to like clarity. But investors who approach this moment expecting a single trade agreement to transform India's outlook overnight are likely to be disappointed. India's opportunity set has never hinged on one export channel or bilateral relationship. Its strength, and its complexity, come from scale, domestic demand and the gradual compounding of reforms.

Seen through that lens, the trade deal is best understood as confirmation, not creation.

The timing matters. Indian equities entered this moment after a period of adjustment. Global risk aversion, currency pressure and trade frictions weighed on performance, and foreign portfolio investors reduced exposure. Yet that selling pressure was largely absorbed by domestic investors, with participation in systematic investment plans reaching record highs.2

Crucially, many of the policy supports investors typically wait for were already in place. Income tax reductions and Goods & Services Tax (GST) relief were implemented well ahead of the most recent budget cycle,3 supporting household balance sheets and consumption before trade headlines improved. Volatility did not derail the underlying economic trajectory, but it tested investor patience.

This backdrop helps explain why the trade deal resonated so quickly. It arrived not as a rescue, but as validation.

Looking ahead, the more durable drivers of India's growth story remain domestic, and increasingly visible.

One reason the trade deal should be interpreted carefully is that India is not an export-led economy in the traditional emerging-market sense. Domestic consumption, services and investment drive growth.7 This makes trade agreements accretive rather than existential.

It also affects currency dynamics. The Indian rupee remains sensitive to oil prices and precious-metal imports, particularly gold and silver. However, improved trade clarity, sustained growth and a stable capital account provide counterweights. A modestly stronger currency need not undermine India's economic engine in the way it might elsewhere.

For many global investors, India is still framed through narrow stereotypes: outsourcing, call centers or low-cost IT services. Those segments are evolving, and in some cases shrinking, as artificial intelligence reshapes global labor markets.8 Yet the broader picture is more nuanced.

Global firms continue to expand higher-value operations in India, domestic companies are moving up the manufacturing and technology stack, and sectors such as defense, autos, pharmaceuticals and financial services are becoming increasingly relevant to both domestic and international markets.

India's equity market composition reflects this diversification more than is often assumed.

Ultimately, the U.S.–India trade agreement is important precisely because it is not the whole story. It removes a layer of uncertainty, reinforces India's strategic relevance and supports a growth trajectory that was already in motion.

For investors, the takeaway is straightforward: India's long-term case does not rest on a single deal, election or quarter of performance. It rests on compounding, including that of policy, capital and participation.

The trade deal didn't change that path. It simply made the direction clearer.

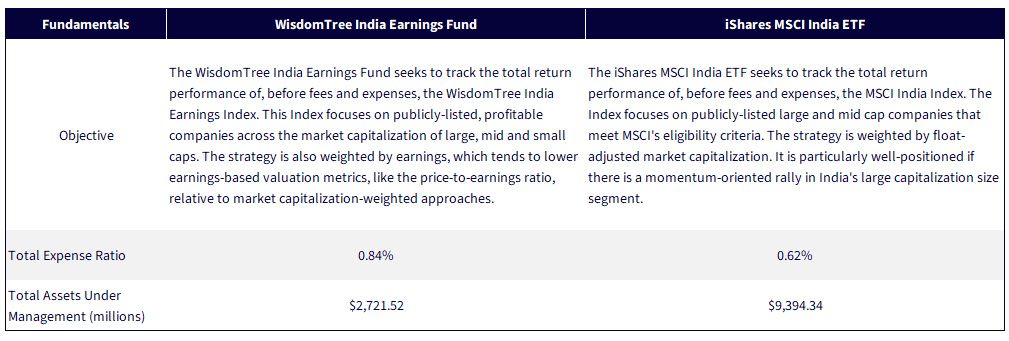

Macroeconomic narratives matter, but ultimately they must be tested in markets. India's evolving economic structure, driven by domestic demand, policy continuity and rising capital formation, shows up not just in growth forecasts, but in how equities perform and how that performance is distributed across strategies. To ground the discussion, it is useful to look at India through three complementary equity lenses:

Together, these perspectives help distinguish India-specific dynamics from broader emerging-market trends, and clarify where recent performance is cyclical versus structural.

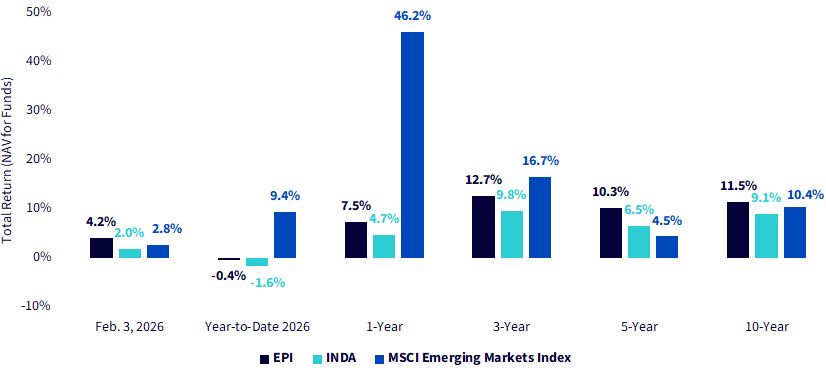

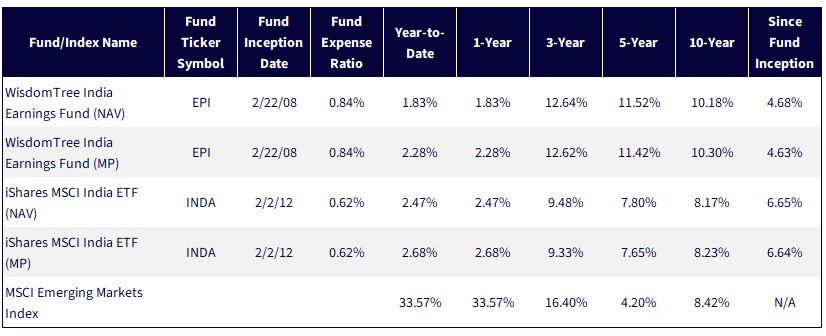

In Figure 1a, we can note what has been characterized as a reaction to initial ‘trade-deal' announcements within the February 3, 2026 performance, and that this is following some near-term underperformance of India's equities relative to that of the broader MSCI Emerging Markets Index. We think it's important to try to account for both the short, medium and long-term trends for a better overall understanding of how a more volatile market, like India, may be doing.

Figure 1a: Gauging Long & Short-Time Horizon Performance

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of February 4, 2026, but showing returns for the period ended February 3, 2026 for Figure 1a and December 31, 2025 for 1b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted.For the most recent month-end and standardized performance, click the relevant ticker:EPI, INDA.

India's recent momentum is best understood not as a reaction to a single catalyst, but as the result of compounding forces moving in the same direction. Policy continuity, domestic demand and improving balance sheets created the foundation; the trade deal helped clarify the path forward. Equity performance now reflects those dynamics in different ways, depending on how investors choose to access the market. For long-term allocators, the key question is less about timing the next headline and more about recognizing when uncertainty has meaningfully declined. In that context, India increasingly looks less like a tactical emerging-market trade, and more like a durable, structurally differentiated allocation.

Sources: WisdomTree and iShares. Assets under management as of February 3, 2026.

1 Sources: U.S. Trade Representative. (2026). India | U.S. Trade Representative: Countries & Regions; U.S. Trade Representative. (2025). Fact Sheet: U.S.–India Establish Terms of Reference on Bilateral Trade; Chaudhary, R. (2026). U.S.-India trade deal: Phase one of bilateral trade agreement almost complete. LiveMint.

2 Source: India Brand Equity Foundation. (2025). Foreign Institutional Investors (FII) and Domestic Institutional Investors (DII) equity flows in India.

3 Source: Economic Times. (2025, September 21). Income tax exemption, combined with GST reforms, will result in savings of Rs 2.5 lakh crore (PTI). Economic Times.

4 Source: Times of India. (2026, February 1). India Inc backs Union Budget 2026 push on manufacturing, infra and competitiveness. Times of India.

5 Source: Times of India, 2026.

6 Source: Reserve Bank of India. (2024). Gross NPAs of banks decline to 12-year low of 2.6%: RBI report (as reported in The Economic Times). The Economic Times.

7 Source: The Economic Times. (2025, May 31). India's GDP growth surges to 6.5% in FY25 led by domestic consumption and government investment. The Economic Times.

8 Source: Deloitte. (2025). The outsourcing compass: Decoding strategies of today.

9 Refers to the WisdomTree India Earnings Index, which weights profitable companies of India by their earnings. EPI is designed to track the total return performance of this index, after fees and expenses.

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. This Fund focuses its investments in India, thereby increasing the impact of events and developments associated with the region, which can adversely affect performance. Investments in emerging, offshore or frontier markets such as India are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. The Fund invests in the securities included in, or representative of, its Index regardless of its investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

India Earnings Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.

Director, Quantitative Research

Ayush Babel is the Director of Quantitative Research in WisdomTree's multi-asset quantitative research and index teams. In this role, he focuses on developing innovative quantitative strategies across various asset classes while supporting WisdomTree's diverse range of products. His expertise spans factor exploration, portfolio construction and optimization, quantitative investment research, and product development.

With over a decade of experience in the financial services industry, Ayush has held investment research roles at J.P. Morgan and Franklin Templeton. At these institutions, he was responsible for developing and managing equity and fixed income smart beta products, as well as cross-asset risk premia solutions for global institutional and retail clients. His experience covers a broad spectrum of asset classes and investment styles.

Ayush holds a bachelor's in Engineering Physics and a master’s degree in Nanoscience from the Indian Institute of Technology, Bombay.