Inflation Now Taking a Back Seat

Published September 4, 2024

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Key Takeaways

- The Federal Reserve is now prioritizing labor market data over inflation in its decision-making process.

- Inflation remains relevant, but as long as disinflation continues, the Fed can focus more on employment.

- Current core inflation measures are above the Fed’s 2% target, but rate cuts are expected to proceed as long as disinflation persists.

With Labor Day now in the rearview mirror, the money and bond markets will no doubt become laser focused on the September FOMC meeting. Yes, Fed Chair Powell telegraphed that a rate cut is forthcoming, but he also emphasized how monetary policy is still data dependent. This data dependency is no longer determining if/when a rate cut could be coming, but rather, it plays the key role in what the looming easing cycle will look like. Based on Powell & Co.’s recent remarks, the number one focus in the Fed’s dual mandate of inflation and employment will now apparently be flip-flopped. In other words, inflation will be taking a back seat to future labor market data.

Now, does that mean inflation has fallen completely off the FOMC’s radar? No, not at all. As long as the current disinflation trend remains intact, the policy makers can tilt their focus more to the employment aspect of their dual mandate. In fact, based on recent Fedspeak, one gets the sense there is some anxiety about the labor market cooling too much.

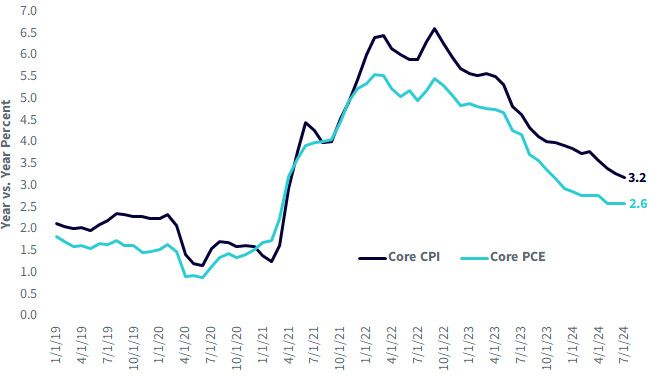

Core Inflation

Source: Bloomberg, as of 8/30/24.

But, what about inflation? It has become increasingly apparent the Fed will not come anywhere close to their 2% target as rate cuts get underway. And I’m not just talking about the first cut either. Given where current core inflation measures reside, it seems obvious that the rate cut process will be in full swing as long as there is not a reversal of the disinflation trend whereby price pressures re-emerge.

Let’s take a look at the two closely watched core inflation gauges to get some perspective. Through July, the latest data available, core CPI, was still increasing at a 3.2% annual rate while the Fed’s own preferred measure, the core PCE deflator, was rising at a 2.6% year-over-year clip. Interestingly, the core PCE reading is below the Fed’s most recent median estimate of 2.8% for 2024, but it is still measurably above their stated goal of a 2% target. In fact, the annualized gain for core PCE has remained at this 2.6% pace for three months in a row.

Conclusion

Pre-Jackson Hole, that type of inflation outcome would have more than likely been viewed through a different prism by the money and bond markets. However, post-Jackson Hole, the Treasury arena now knows what the primary driver is for future Fed policy decision-making: jobs, jobs, jobs.

Categories

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.