Inside the Playbooks: How the Giants Are Executing AI

Published August 27, 2025

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- In 2025, the Magnificent 7 continue to dominate AI narratives, but diverging strategies, from Nvidia’s chip supremacy to Alphabet’s consumer integration, reveal a broader playbook of AI execution.

- Amid rising capital expenditures and intensifying competition, companies like Microsoft and Amazon are proving they can monetize AI across infrastructure and applications, translating hype into cash flows.

- The WisdomTree U.S. Quality Growth Fund (QGRW) offers a fundamentals-based filter to access AI leaders like Broadcom and Meta, balancing sector growth potential with disciplined profitability.

AI at Scale: How the World's Largest Companies Are Executing the Next Industrial Revolution

Every era of markets has its icons. In the 1980s, it was the oil majors. In the 1990s, it was telecom and dot-com darlings. Today, we live in the age of the Magnificent 7—companies so large that their combined market value exceeds the gross domestic product (GDP) of most nations, and so central to the story of artificial intelligence (AI) that one cannot talk about AI without them. Their share prices are a daily referendum on whether AI is considered hype or reality. Each earnings release is less about quarterly profits and more about the trajectory of machine intelligence, cloud dominance or chip design. Investors, policy makers and competitors alike read their moves as signals about where the global economy is heading.

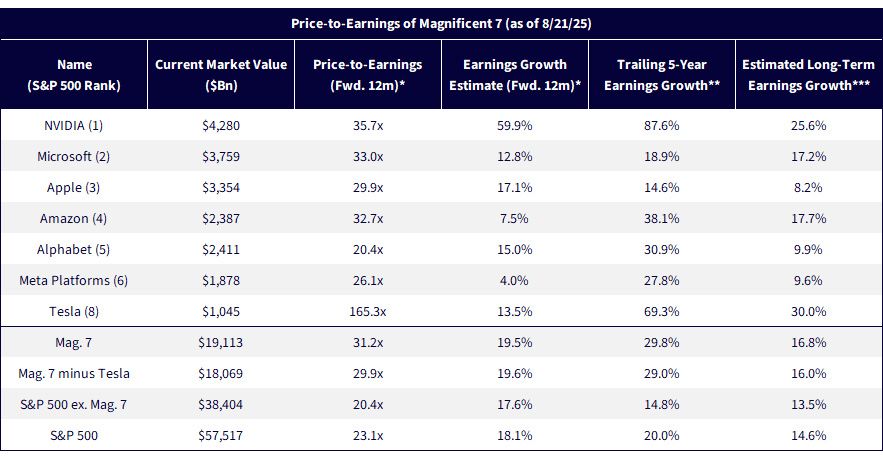

Figure 1 brings the Magnificent 7 into sharp relief: their size, their valuations and the growth expectations embedded in their stocks.

- The Magnificent 7 are priced as if AI is not just a growth driver, but the growth driver. Their forward price-to-earnings (P/E) multiples, averaging over 31 times, sit well above the broader S&P 500, reflecting investor conviction that these firms hold the keys to the next wave of technological disruption.

- Not all giants are equal in the AI trade. NVIDIA's blistering earnings growth expectations stand in sharp contrast to Meta's muted outlook or Tesla's sky-high multiple, reminding us that the market is simultaneously betting on proven profit engines, moon shot visions and everything in between.

Figure 1: AI at Scale: How the Giants Are Priced for Growth

Sources: WisdomTree, FactSet, S&P. *Calendar year price-to-earnings and earnings growth based on median analyst estimates. **Trailing 3-year where 5-year is not available. Growth is annualized ***Estimated Long-Term Growth is annualized and based on median analyst earnings growth estimates over the next 3 years. Trailing 5-year Earnings Growth and Estimated Long-Term Earnings Growth as of 7/31/25. All other data as of 8/21/25. Aggregate metrics shown as weighted averages. You cannot invest directly in an index.

A Smarter Path to Growth

The WisdomTree U.S. Quality Growth Fund (QGRW) was built on a simple but powerful premise: inclusion should be earned through fundamentals, not simply inherited by market size. Unlike the Nasdaq 100 Index, which mechanically collects the largest non-financial companies trading on that exchange,1 QGRW draws its membership from a rules-based Index that emphasizes profitability, return on equity and earnings quality. The result is a portfolio that tilts toward companies demonstrating not only scale, but the discipline and durability to sustain it. In an era where market darlings are often anointed by narrative—AI being the latest example—QGRW offers investors a systematic way to potentially separate enduring leaders from more temporary winners.

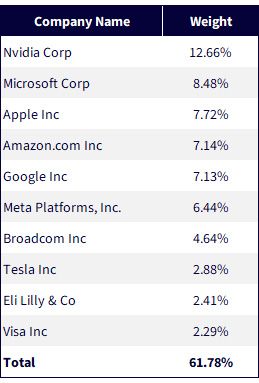

Figure 2 shows the top 10 positions in QGRW:

- AI is the foundation. The Magnificent 7 appear among QGRW's top holdings, reflecting the Fund's quality-growth methodology naturally pulling in the very companies leading the global AI race.

- Quality filters sharpen the AI exposure. Alongside the giants, holdings like Broadcom, Eli Lilly and Visa provide diversified ballast, ensuring AI exposure remains grounded in fundamentals.

Figure 2: The Quality Growth Leaders Defining the Future

Source: WisdomTree, with data as of 8/21/25. Subject to change.

Inside the Playbooks: How the Giants Are Executing AI

Owning the leaders is one thing, but understanding how they are leading is another. The companies at the core of QGRW are not simply beneficiaries of AI enthusiasm; they are the architects of its future. NVIDIA builds the chips, Microsoft deploys the software, and Alphabet and Amazon weave AI into their vast ecosystems, while Meta, Tesla and Broadcom push the boundaries of new applications. Each firm's approach reflects a different philosophy of scale, risk and execution. To see where AI is truly heading, we need to open the hood on these strategies and evaluate how effectively they are being translated into real-world growth.

Alphabet2

Alphabet has moved beyond "catch-up" and is now differentiating itself in consumer-facing AI. Gemini is integrated across Pixel 10 devices, Workspace, YouTube and Chrome—embedding AI not as an app but as daily utility. Pixel adoption remains modest in share terms, but as a proof point it validates Alphabet's ability to move AI to the device level with features like Magic Editor and live translation. Google Cloud AI bookings are growing by more than 35% year over year, and Workspace now has more than one billion paid and free users feeding the data flywheel. Alphabet's proprietary Tensor Processing Unit (TPU) v5p chips, already deployed at hyperscale, cut inference costs by approximately 40% relative to graphics processing unit (GPU) peers, giving it cost leverage competitors can't easily replicate.

Financially, Alphabet is guiding to 13% or more topline growth3 in 2025, with ad revenue stable and cloud approaching a $50 billion annualized run-rate. EBITDA4 margins are expanding into the mid-30s, even as capital expenditures rise 40% to fund AI data centers. Trading at approximately 20 times forward earnings—very similar to the multiple on the S&P 500 Index—investors are paying for stability, not optionality. Yet optionality exists. Consumer AI adoption, TPU scaling and rapid iteration cycles (Gemini 2.0 to 2.5 in six months) all suggest accelerating monetization. Alphabet is an overlooked AI compounder—bridging foundational research, consumer adoption and hyperscale economics with a valuation that doesn't reflect the optionality.

Microsoft5

Microsoft's AI edge lies in touching every layer of the stack. Azure AI workloads are expected to contribute 25% of Azure revenue by fiscal year 2026, led by OpenAI services, Fabric (growing by more than 50% year over year) and third-party workloads like Snowflake migrations. Copilot penetration is climbing. Early surveys suggest more than 30% of Fortune 500 enterprises have budgeted for Copilot in 2025, echoing the E3/E56 upgrade cycle that re-rated Microsoft's Software as a Service (SaaS) growth in the 2010s.

Financials underscore the breadth: fiscal year 2025 revenue up 15% and Intelligent Cloud up 21%, with capital expenditures up 58% to approximately $88 billion. Despite that spend, operating margins expanded as higher-margin AI workloads offset infrastructure costs. Earnings per share is expected to double from fiscal year 2024–28, with SaaS monetization and AI upgrades the key drivers. Free cash flow remains above $60 billion annually, funding both capital expenditures and buybacks.

With a $3.8 trillion market cap and mid-30s P/E, Microsoft is not cheap—but visibility is high. It is monetizing AI at both the infrastructure (GPU cycles, data workloads) and application layers (Copilot across Office, Teams, Dynamics7). For investors, this is AI monetization without mystery: proven cash flows tied to adoption, making Microsoft both toll collector and productivity engine of the AI economy.

Amazon8

Amazon approaches AI as system integration. Across retail, more than 1,000 active AI projects are reshaping demand forecasting, personalization and logistics. Rufus, the conversational shopping assistant, and Amazon Lens are showing early traction, while AI-enabled robotics—over 1 million robots deployed—are reducing logistics costs by 10%–15%. Prime Air drones, reapproved in 2025, now serve test markets with AI-powered obstacle detection.

Amazon Web Services (AWS) remains the cornerstone. AI workloads account for more than 40% of incremental demand, with Bedrock simplifying access to foundation models and Titan extending proprietary options. AWS AI services revenue is growing by more than 30% year over year, with gross margins above 30%, sustaining double-digit EBITDA growth even as capital expenditures rise. Zoox robotaxi pilots in San Francisco and Las Vegas position Amazon in future mobility, but the near-term win is AWS consolidation as the default AI partner for corporates.

Financially, retail margins are climbing as AI reduces fulfillment costs, while AWS remains a cash machine. Amazon trades in the low-30s P/E range, with growth optionality from both commerce AI and AWS scale. For investors, Amazon offers a dual AI story of invisible productivity dividends across retail, and cloud leadership that sells AI to everyone else.

Meta Platforms9

Meta's AI strategy is built on compounding engagement and monetization while funding frontier bets. Recommendation engines are driving 5%–6% sequential increases in time spent, while GEM10 and Andromeda ad systems deliver 3%–5% better conversions per iteration—powerful lifts when applied to a $200-billion-plus revenue base. AI also powers new features like multimodal search in Instagram, further boosting stickiness.

Financially, revenues are growing 20% in 2025, earnings per share are expected to grow nearly 40% between 2024 and 2026. Capital expenditures will surpass $100 billion in 2026, largely directed toward data center expansion and compute capacity. Despite Reality Labs losses, operating cash flow from ads more than covers investments. Meta trades in the mid-20s P/E, balancing short-term ad compounding with long-term AI moon shots.

The frontier bet is Meta Superintelligence. Hyperion, a 2GW compute cluster in Louisiana, reflects CEO Mark Zuckerberg's ambition to out-build rivals. Coupled with aggressive talent acquisition, Meta is trying to collapse the reasoning gap exposed in Llama 4. For investors, the company offers a dual narrative of near-term efficiency gains monetized at scale, and long-term optionality in frontier AI. This blend makes Meta both a margin machine today and a speculative infrastructure builder for tomorrow.

Apple11

Apple's AI narrative is ecosystem-first. Apple Intelligence, launched with iOS 18, enables summarization, multimodal editing and context-aware Siri across iPhones, iPads and Macs. Adoption is subtle—users are not "choosing AI"—they are choosing convenience. Surveys show approximately 30% of iPhone upgraders cite Apple Intelligence features as a purchase driver, hinting at accelerated refresh cycles.

Financially, Services revenue is now more than $120 billion annually, aided by AI-driven upsell in iCloud+ and AppleCare. Hardware margins hold above 45%, supported by proprietary neural engines that reduce reliance on Nvidia GPUs. Apple's capex efficiency—spending less than half of Microsoft or Meta on AI—underscores its integrated model.

Apple trades at a valuation below peers but with growth optionality embedded in every device cycle. The strategy is less about headline breakthroughs and more about quietly turning AI into annuities across services, devices and ecosystems. For investors, Apple represents the consumer distribution monopoly in AI—where billions of micro-decisions flow through one vertically integrated stack.

Tesla12

Tesla's AI pivot emphasizes fleet intelligence and robotics. With Dojo13 scaled down, Tesla now leans on Nvidia and Advanced Micro Devices (AMD) for training but focuses on deployment; millions of cars as distributed inference nodes. Full Self Driving attach rates in North America rose 25% in 2025, creating a recurring revenue stream layered on top of auto sales. Robotaxis are operational in Austin, with expansion underway.

Financially, second-quarter 2025 margins exceeded expectations—Automotive at 15%, Energy at 30%—with total revenue at $22.5 billion. Energy storage deployments are also scaling, benefiting from AI-driven optimization. Optimus, the humanoid robot, remains speculative but is slated for 2026 ramp, with CEO Elon Musk reiterating targets of more than one million units within five years.

Tesla trades at a very high multiple of earnings—an asymmetric bet on AI mobility and robotics. Execution risks (Chinese electric vehicle competition, regulatory hurdles, factory ramps) are real. Yet Tesla remains the purest play on embodied AI: a company turning distributed intelligence into economic infrastructure, with optionality spanning transport, energy and labor.

Nvidia14

Nvidia is still the gravitational center of AI. Its Blackwell GPUs dominate hyperscaler demand, Rubin is queued for 2026 and CUDA15 keeps developers locked in. Sovereign AI16 revenues are greater than $12 billion in FY25, diversifying exposure beyond U.S. hyperscalers and offsetting lost China sales. Of course, we continue to monitor efforts and execution at selling H20's into China, an action only approved more recently by the U.S. government, but possibly offset by China's government discouraging their use.

Nvidia's financials remain unmatched: fiscal year 2025 revenue at $130 billion (+114% year over year), gross margins above 70%, operating margins above 60%. Free cash flow is compounding even as research & development (R&D) surpasses $20 billion annually. By fiscal year 2027, revenues are projected to be above $260 billion. Risks include hyperscaler ASIC17 adoption and export restrictions, but Nvidia's ecosystem remains irreplaceable.

At approximately 35 times forward earnings, Nvidia trades at a premium—but with growth that justifies it. It is not just a chipmaker; it is the toll operator of AI. For investors, Nvidia remains the default bet on the buildout of machine intelligence infrastructure.

Broadcom18

Broadcom has quietly become indispensable to AI infrastructure. Networking revenues grew 170% year over year in 2025, with Ethernet now 40% of AI-related sales. Management expects processors to take a greater share as Google and Meta refresh ASIC deployments.

April 2025 revenue hit $15 billion (+20% year over year), with semiconductor up 16% and infrastructure software up 25%. VMware integration is exceeding expectations, with 87% of top customers adopting the full stack. Gross margins are nearly 80%, providing resilience in an arms race where others are burning cash.

AI revenues could reach $30 billion by 2026, consistent with a $60–$90-billion total addressable market by 2027. At approximately 40 times forward earnings, Broadcom is rewarded for stability and diversification. For investors, it is the uncontroversial AI winner—monetizing growth by being the indispensable connective tissue of the AI datacenter.

Conclusion: A Quality-Growth Lens on AI

The Magnificent 7 dominate the narrative around AI, and we also add in Broadcom in this piece as an important player, but their strategies and trajectories diverge widely.

What QGRW offers is a way to harness this transformative trend through a fundamentals-driven filter: exposure to the companies that are not just large, but disciplined in profitability and growth. In an environment where narratives shift quickly, the combination of AI leadership and financial rigor may be the smarter path to long-term compounding.

1 Source: "NASDAQ100 Index Methodology," Nasdaq, Inc., 2025.

2 Sources for the Alphabet section: Morgan Stanley Research, "Alphabet Inc. (GOOGL.O): AI-Driven Acceleration; Remain Overweight," Morgan Stanley, 7/24/25; Goldman Sachs Global Investment Research, "Alphabet Inc. (GOOGL): Made by Google 2025—Launch of New Pixel Hardware Emphasizes Scaling of Gemini AI Utility," Goldman Sachs, 8/20/25; Goldman Sachs Global Investment Research, "Google Pixel Report: Scaling Gemini AI Utility through Consumer Hardware," Goldman Sachs, 8/20/25.

3 Topline refers to the top of the income statement, revenues.

4 EBITDA refers to earnings before interest, taxes, depreciation and amortization.

5 Sources for Microsoft section: Morgan Stanley Research, "Microsoft Corporation (MSFT): FY25 Results—AI Scaling across Cloud and Productivity," Morgan Stanley, 7/31/25; K. Rangan et al., "Microsoft Corp. (MSFT): The AI Halo Effect Ripples Up the Stack—F4Q25 Earnings," Goldman Sachs, 7/31/25.

6 E3 (Enterprise 3) and E5 (Enterprise 5) are subscription bundles for Microsoft 365 (formerly Office 365), aimed at enterprise customers.

7 A cloud-based business applications platform, launched in 2016 by merging Microsoft Dynamics AX (ERP) and Dynamics CRM into one SaaS offering.

8 Sources for the Amazon section: B. Nowak et al., "Amazon.com Inc. (AMZN): Retail Delivers, AWS Acceleration on Deck," Morgan Stanley, 8/1/25; E. Sheridan et al., "Amazon.com Inc. (AMZN): Q2'25 Review—Solid eCommerce Growth & Margins; Debate Likely to Remain Centered on AWS vs. AI Market Narratives," Goldman Sachs, 8/1/25.

9 Sources for the Meta Platforms section: Morgan Stanley Research, "Meta Platforms, Inc. (META): AI Engagement Lifts Core, while CapEx Points to Supercomputing Scale-Up," Morgan Stanley, 7/31/25; E. Sheridan et al., "Meta Platforms Inc. (META): Q2'25 Review—Sustained Core Business Strength Fuels Long-Term Growth Investments," Goldman Sachs, 7/31/25; D. Patel et al., "Meta Superintelligence—Leadership Compute, Talent, and Data," SemiAnalysis, 7/11/25.

10 In the context of Meta Platforms, GEM refers to an AI-powered advertising system the company has rolled out in recent years to optimize ad performance across its platforms (Facebook, Instagram, Messenger, WhatsApp).

11 Sources for Apple section: E.W. Woodring et al., "Apple Inc. (AAPL): iPhone Build Revisions Higher; Potential AI Partnership a Catalyst," Morgan Stanley, 8/14/25; E.W. Woodring et al., "Apple Inc. (AAPL): June Q Results—Resilient Services and Early Apple Intelligence Traction," Morgan Stanley, 8/1/25; M. Hall et al., "Apple Inc. (AAPL): F3Q25 Review—Resilient Results; Apple Intelligence to Drive Ecosystem Monetization," Goldman Sachs, 8/1/25.

12 Sources for the Tesla section: A. Jonas et al., "Tesla Inc. (TSLA): EV Pain vs. Robo Gain—Crossing the Chasm to Autonomy," Morgan Stanley, 7/24/25; A. Jonas et al., "Tesla Inc. (TSLA): Robonomics, Nukes on the Moon, the Elon Quotient," Morgan Stanley, 8/7/25; A. Jonas et al., "Tesla Inc. (TSLA): Dojo Gets DOGE'd? 5 Key Thoughts on Scaling Back Custom Silicon," Morgan Stanley, 8/10/25; E. Sheridan et al., "Tesla Inc. (TSLA): Q2'25 Review—Near-Term Pressures but Long-Term AI/Robotics Optionality Intact," Goldman Sachs, 8/1/25.

13 Dojo refers to the company's in-house supercomputer project designed specifically for training its AI models, with the ultimate goal of enabling Full Self Driving (FSD), Optimus humanoid robots and other autonomous systems.

14 Sources for the Nvidia section: J. Moore et al., "NVIDIA Corp. (NVDA): Earnings Preview—Setting Up for a Very Strong 2026," Morgan Stanley, 8/18/25; T. Hari, "Semiconductors: Nvidia's Outlook and Competitive Positioning—Blackwell Ramp, Inference Demand, and Ecosystem Stickiness," Goldman Sachs, 8/18/25; A. Alper, "Nvidia CEO in Taipei to Visit TSMC, Says in Talks with U.S. over New China Chip," Reuters, 8/22/25; "‘My main purpose coming here is...': CEO Jensen Huang Visits Taiwan as Nvidia Looks to Stop H20 AI Chips Production," The Times of India, 8/22/25.

15 CUDA (Compute Unified Device Architecture) is Nvidia's proprietary parallel computing platform and programming model, introduced in 2006. It allows developers to harness the power of Nvidia GPUs for general-purpose computing (not just graphics).

16 Refers to sales to governments.

17 ASIC refers to application specific integrated circuits.

18 Sources for the Broadcom section: J. Moore et al., "Updating AI Semis Price Targets: Broadcom, Nvidia, AMD, Marvell, and Astera Labs," Morgan Stanley, 7/30/25; J. Moore et al., "Broadcom Inc. (AVGO): Strong AI Networking Drives in Line Results but Higher CY26," Morgan Stanley, 6/6/25.

Important Risks Related to this Article

For current holdings of QGRW, please click here. Holdings are subject to risk and change.

There are risks associated with investing, including the possible loss of principal. Growth stocks, as a group, may be out of favor with the market and underperform value stocks or the overall equity market. Growth stocks are generally more sensitive to market movements than other types of stocks. The Fund is non-diversified, as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit. The Fund does not attempt to outperform its Index or take defensive positions in declining markets and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.