WTAI

Artificial Intelligence and Innovation Fund

Published June 4, 2026

Global Head of Research

There is a phrase circulating with increasing frequency in conversations about AI infrastructure:

The bottleneck.

Compute—specifically graphics processing units (GPUs)—was the dominant variable in AI progress during the early years of AI, but it has become abundant enough that new constraints have moved to the foreground. The limitation today is less often whether a model can run and more often whether:

These are engineering problems masquerading as investment themes, and identifying which strategies have oriented themselves toward the genuine constraints, as opposed to the general excitement around AI, is now one of the more meaningful distinctions in thematic investing.

Two bottlenecks dominate the current conversation:

2. Memory bandwidth and capacity

High-bandwidth memory, or HBM, has become the critical substrate for GPU performance. When Nvidia ships an H100, a Blackwell or a Rubin system, the memory that determines how fast it can operate typically comes from SK Hynix, Micron or Samsung. Storage more broadly, like the NAND flash from the companies that became SanDisk and Kioxia, feeds the data pipelines that AI training and inference consume continuously.

2. Optical networking

This represents the fiber, transceivers, and switching equipment that move data between GPUs at the speeds AI workloads require. Companies like Lumentum, Coherent, Corning, and Credo Technology are building the connective tissue of the AI data center, and the demand signal coming from hyperscalers has been among the strongest in the hardware ecosystem over the past two years.

Software?

Software, by contrast, is not a bottleneck in this sense. It is an opportunity, a competitive arena, and it could be a platform for monetization, but it is not the scarce resource. The observation is not a slight against software companies; it is simply a structural point about where AI's scaling constraints actually live in 2026.

Against this backdrop, three AI-oriented ETF strategies offer instructive contrasts.

WTAI has positioned itself most explicitly around infrastructure and bottleneck exposure. As of May 29, 2026, major exposures included Micron (4.70%), Samsung Electronics (4.55%), Nvidia (4.23%), Broadcom (3.36%), SanDisk (3.19%), and Kioxia (3.18%). Together, the memory complex alone represents a substantial plurality of assets. The optical networking thesis also appears with names like Lumentum (2.02%), Coherent (1.69%), Corning (1.23%), Credo Technology (1.18%), and Ciena (0.63%), each of which derives meaningful revenue from AI data center buildout. The pattern across the fund is consistent, placing exposure in companies that supply the physical and semiconductor infrastructure that AI requires to actually function, rather than companies that build applications on top of it. Software and consumer-facing platforms are notably slimmed down in exposure to only the highest conviction names.

BAI, an actively managed strategy, takes an approach that recognizes the bottleneck thesis but holds it alongside a broader AI growth bet. SK Hynix led the fund at 7.4%, followed by Broadcom (5.48%), Micron (5.40%) and AMD (5.03%). The optical networking layer appeared through Lumentum (2.69%), Fabrinet (2.05%), and Credo (1.83%). BAI also carried allocations to Snowflake (1.64%) and Palantir (1.10%). Being actively managed, BAI appears designed to capture both the infrastructure constraint narrative and the software monetization narrative simultaneously, accepting the tradeoff that might come with that breadth.

AIQ, as of this moment in time, had taken the widest view. First, it is tracking the total return performance, before fees and expenses, of the Indxx Artificial Intelligence & Big Data Index, which selects companies from developed markets, plus China-domiciled ADRs/GDRs,2 that demonstrate direct, meaningful exposure to AI. Candidates are sorted into two buckets:

Each company receives a proprietary "Exposure Score" based on how central AI is to its business, and only those clearing a positive score threshold are eligible. Weighting is modified market-cap with individual security caps of 3% (or 1% for lower-scoring names). The index is rules-based with no discretionary committee cited in the methodology.

SK Hynix (7.12%) and Micron (5.76%) were the largest holdings by weight, and Samsung Electronics (4.79%) was also significant. Alphabet (2.72%), Meta Platforms (2.30%), Microsoft (2.35%), Netflix (2.43%), Amazon (2.73%), Apple (2.97%), Salesforce (1.31%), Tesla (2.29%) and Palantir (2.23%) also constitute a substantial portion of the portfolio, and they represent something different from what we might think of as ‘bottlenecks’. Fujikura (0.39%), the Japanese optical fiber manufacturer, and Marvell Technology (1.27%) did appear as less substantial positions. Of the three strategies in this piece, AIQ is effectively a broad technology strategy with an AI narrative, which may serve investors seeking wide exposure to how AI reshapes the economy, but it is a different bet than the infrastructure thesis.

The distinction matters because the bottleneck thesis and the AI adoption thesis can diverge sharply in performance over specific periods. When the market focuses on AI capex cycles and infrastructure spending, memory and optical names tend to lead. When attention shifts to monetization, software multiples could expand. Knowing which thesis a given fund is actually expressing is the starting point for any honest evaluation.

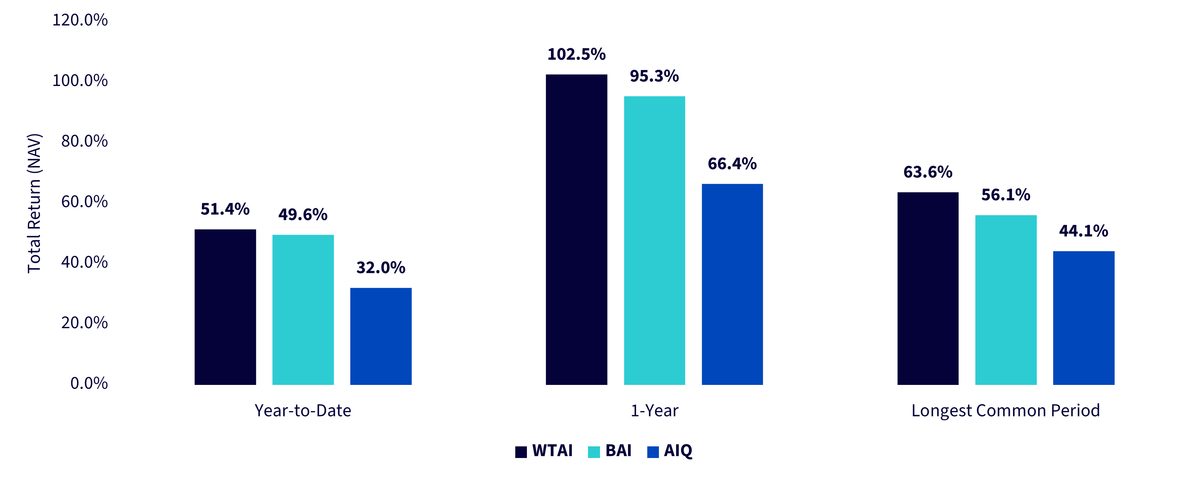

Conclusion: Who is Leading in Terms of Performance?

To be fair, we have to note that performance in this space can be volatile. We are looking at a snapshot as of May 29, 2026. The future is unknown. What’s clear, particularly in the year-to-date 2026 period, is that WTAI and BAI are dramatically ahead of AIQ. We noted above their focus on what we term ‘the bottlenecks’. AIQ doesn’t ignore the bottlenecks by any means; it simply distributes its weight across a broader set of companies.

It is a short-term period in Figure 1a due to the short, live history of BAI, which only began October 21, 2024.

Figure 1a: The Performance Picture So Far

Figure 1b: Standardized Performance

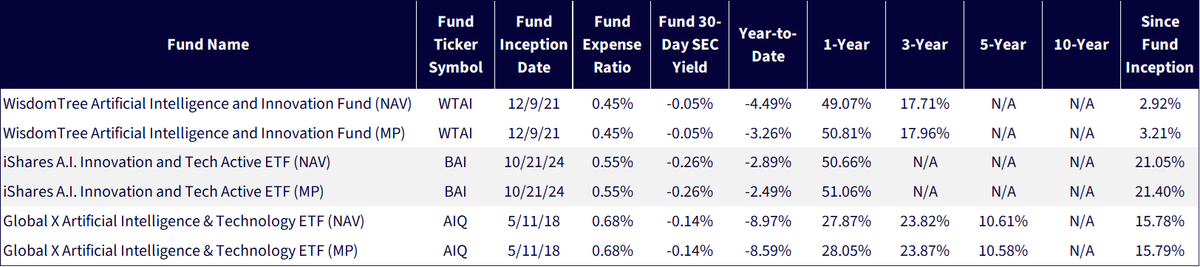

Sources: WisdomTree, FactSet specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed June 1, 2026 with returns as of May 29, 2026 for Figure 1a and March 31, 2026 for Figure 1b. Fund SEC 30-Day Yield as of March 31, 2026. NAV denotes total return performance at net asset value. MP denotes market price performance. Longest Common Period in Figure 1a is governed by the BAI inception date, 10/21/2024. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance and to download the respective Fund prospectuses, click here.

Our bottom line is this—if investors are looking for AI strategies that are ‘minding the bottlenecks,’ we believe the evidence is clear, as of this point in time, regarding where those exposures may be found. If people are focusing on other areas, that is also clear.

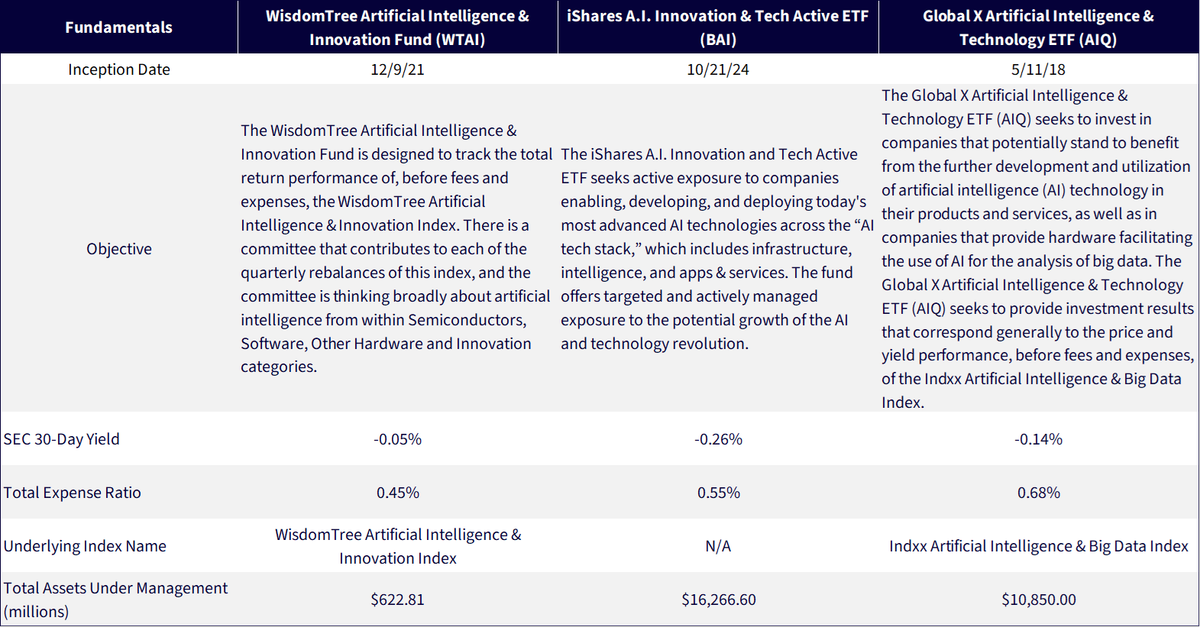

Figure 2: Additional Information

Sources: WisdomTree, iShares and Global X, with data from each respective fund page as of May 29, 2026. Subject to change.

Sources: WisdomTree, iShares and Global X, with data from each respective fund page as of May 29, 2026. Subject to change.

1 Sources: iShares and Global X, specific BAI and AIQ fund pages. Assets under management as of May 29, 2026. Subject to change.

2 ADR stands for American Depository Receipt. GDR stands for Global Depository Receipt.

There are risks associated with investing, including possible loss of principal. The Fund invests in companies primarily involved in the investment theme of Artificial Intelligence (AI) and Innovation. Companies engaged in AI typically face intense competition and potentially rapid product obsolescence. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Additionally, AI companies typically invest significant amounts of spending on research and development, and there is no guarantee that the products or services produced by these companies will be successful. Companies that are capitalizing on Innovation and developing technologies to displace older technologies or create new markets may not be successful. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Artificial Intelligence and Innovation Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.