AIVL

U.S. AI Enhanced Value Fund

Published June 16, 2025

Global Head of Research

The story of U.S. equities in 2025 is not so much a tale of straight lines and logical outcomes, but one of reversals, contradictions and emotional exhaustion. In April, the market dropped 12% in four days after a sweeping round of tariffs was announced—only to roar back just as violently when that same policy was walked back weeks later.1 If markets are a reflection of collective psychology, then we are confused, scared and whiplashed. And in that type of environment, the appeal of value—steady, boring, profit-now value—starts to quietly grow again.

For years, the market's favorite stories were about speed, scale and software. Growth stocks, particularly in tech, earned their way to the top of the leaderboard by delivering on narratives that stretched far into the future.2 But 2025 feels different. Inflation has lingered longer than central banks hoped. Interest rates are sticky. Fiscal policy is erratic. And perhaps most importantly, investor psychology has shifted. The appetite for speculative future earnings has cooled. People don't just want promises—they want something that actually delivers on fundamentals and expectations today.

Against this backdrop, value stocks have shown signs of life. Not in the headlines, but in the way they've held up when things looked most uncertain. The average S&P 500 Index stock endured a 30% drawdown this year—but many value-oriented names with pricing power, domestic supply chains and lower valuation multiples weathered the storm with less drama.3 When companies can negotiate with suppliers, shift production away from tariffs or simply pass costs along to customers, they become something of a safe harbor. Not flashy, but functional.

There's also a deeper truth that gets lost in the shuffle of earnings reports and macro charts: the value investment style works best when people stop believing anything works.4 It's not about optimism. It's about disillusionment. When the dreamier corners of the market—more speculative and not yet profitable—start to feel fragile, value is what's left. These are companies with earnings, low multiples and stories that don't require perfect macro conditions. They're already priced for disappointment. If things merely turn out "less bad," they can rally.

This isn't a prediction that value will dominate the next decade. But in a year like 2025—marked by economic crosswinds, tariff-induced pricing shocks and investors who can't decide whether to fear missing out or fear getting in—value offers something that's hard to find right now: simplicity. You can understand the businesses. You don't need zero rates or moonshot forecasts. Sometimes, surviving the chaos isn't about doubling down on what used to work. It's about remembering that boring can be beautiful when everyone else is overwhelmed.

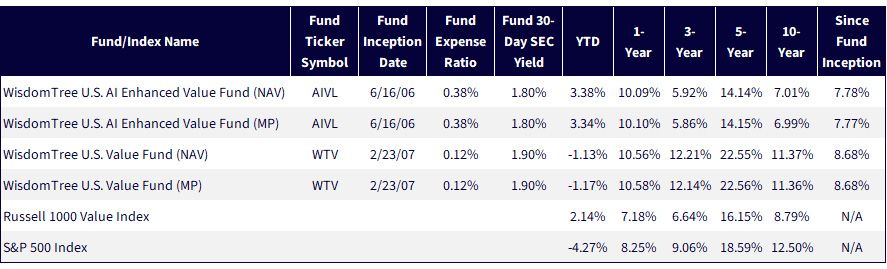

In the evolving landscape of U.S. value investing, WisdomTree has constructed an array of approaches, two of which reflect very different philosophies about how the value investment style can be identified and captured. The WisdomTree U.S. Value Fund (WTV) leans into a traditional—but historically effective—signal: shareholder yield. This strategy emphasizes companies that return capital to shareholders through dividends and buybacks, while simultaneously filtering out so-called "value traps" through a quality and momentum-based risk score. The goal is to isolate firms with sustainable cash generation and disciplined capital allocation—companies that are not only cheap on paper but demonstrably returning value to investors.

On the other hand, the WisdomTree U.S. AI Enhanced Value Fund (AIVL) takes a forward-looking, machine learning-driven approach that challenges conventional definitions of value. Built in partnership with Voya's Equity Machine Intelligence platform, AIVL does not rely on a fixed set of financial ratios. Instead, it leverages over 250 features drawn from fundamental, market, sentiment and alternative datasets to dynamically interpret what constitutes value in different market regimes. The model adapts over time, learning which valuation signals are working and which are not, with the aim of generating timelier and context-sensitive portfolio positioning.

While WTV's construction is more intuitive and often appeals to income-focused investors, AIVL seeks to capitalize on market inefficiencies through dynamic reallocation. The contrast sets the stage for exploring how these strategies may perform differently in environments marked by macro shocks, sector rotations or shifts in investor sentiment.

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 5/29/25, with returns as of 3/31/25. NAV denotes total return performance at net asset value. MP denotes market price performance. AIVL's objective and strategy changed effective 1/18/22. Prior to this date, AIVL performance reflects the investment objective of the Fund when it was the WisdomTree U.S. Dividend ex-Financials Fund (DTN) and tracked the performance, before fees and expenses, of the WisdomTree U.S. Dividend ex-Financials Index. In the case of WTV, the Fund's objective changed effective 12/18/17. Prior to this date, Fund performance reflects the investment objective of the Fund when it tracked the performance, before fees and expenses, of the WisdomTree U.S. LargeCap Value Index. The performance data quoted represents past performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: AIVL, WTV.

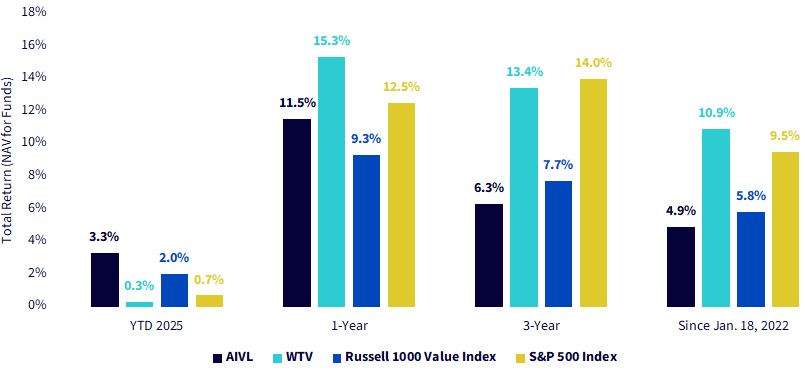

If there's a single chart that reframes the debate on value investing in 2025, it's figure 2. Over one year, three years and even since January 2022—despite a backdrop where growth dominated headlines—WTV has not only kept pace with the S&P 500 Index, it has in some cases beaten it. That's a powerful signal. Too often, value strategies are framed defensively—as a ballast during uncertainty, but rarely a source of leadership. WTV's performance track record has turned that notion on its head. By leaning into shareholder yield and screening out low-quality companies that resemble value traps, it has delivered a fundamentally driven, valuation-aware strategy without lagging one of the most widely followed benchmarks in the world.

By contrast, AIVL has shown behavior more in line with the Russell 1000 Value Index. This isn't a failure—far from it. AIVL is doing what its AI engine was designed to do: track evolving definitions of value in real time, remain benchmark-aware and avoid over-committing to static factors. But what the numbers remind us of is that not all value strategies are built to lead. Some are meant to be adaptive, steady and responsive to changing conditions. WTV, with its clear focus on capital allocation discipline, has shown it can be something rarer: a value strategy that doesn't just avoid underperformance—it challenges for leadership of the U.S. equity market itself over these periods.

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 5/29/25, with returns as of 3/31/25. NAV denotes total return performance at net asset value. MP denotes market price performance. AIVL's objective and strategy changed effective 1/18/22. Prior to this date, AIVL performance reflects the investment objective of the Fund when it was the WisdomTree U.S. Dividend ex-Financials Fund (DTN) and tracked the performance, before fees and expenses, of the WisdomTree U.S. Dividend ex-Financials Index. In the case of WTV, the Fund's objective changed effective 12/18/17. Prior to this date, Fund performance reflects the investment objective of the Fund when it tracked the performance, before fees and expenses, of the WisdomTree U.S. LargeCap Value Index. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: AIVL, WTV.

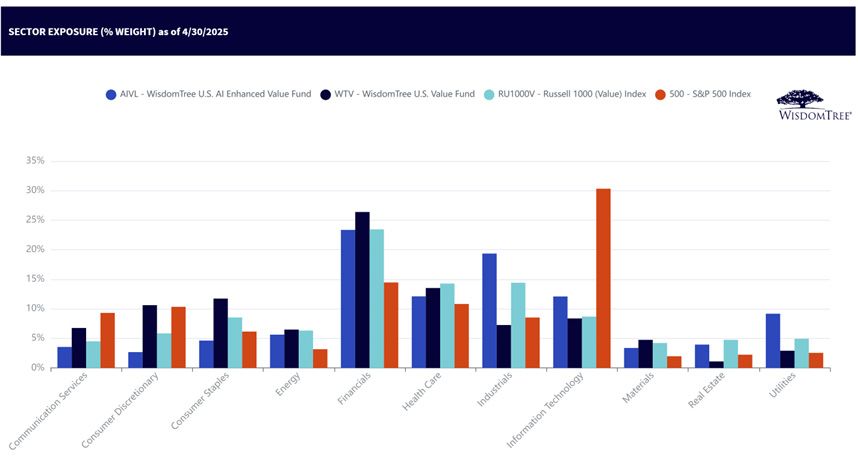

Sector exposures offer a window into what a strategy is implicitly betting on. In figure 3, we see clear divergences between WTV and AIVL that stem directly from their underlying philosophies. WTV's largest overweight is to financials, followed by consumer staples and energy—all classic high-shareholder-yield sectors. These are businesses that often return large amounts of cash to shareholders and tend to show up in portfolios that prize capital return discipline. That aligns perfectly with WTV's methodology, which screens for dividend and buyback yield while seeking to steer clear of value traps.

AIVL, by contrast, leans more heavily into industrials, health care and utilities—sectors where its AI model has likely identified a blend of fundamental strength and attractive valuation characteristics. Its lower exposure to financials and consumer staples suggests a different opportunity set, one driven more by cross-sectional signals across sectors than by a singular factor like shareholder yield. Meanwhile, AIVL's elevated position in utilities, for example, could reflect an AI-identified convergence of stable fundamentals, favorable sentiment and relative value—not a traditional over-weight position you'd see from a rules-based dividend screener.

Sources: WisdomTree, FactSet. Subject to change.

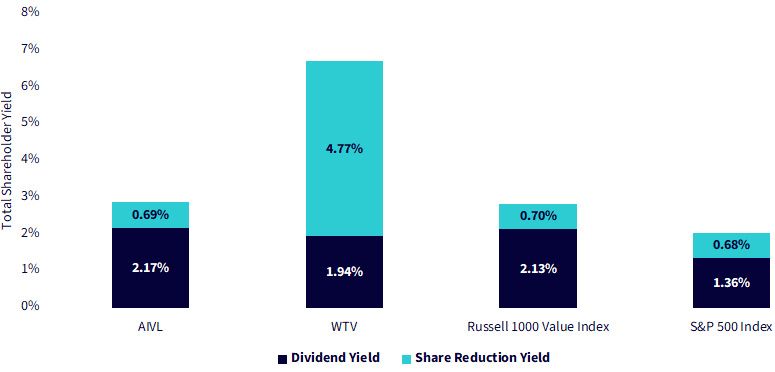

If one metric encapsulates the core difference between WTV and AIVL, it's shareholder yield. As this chart shows, WTV's total shareholder yield is more than double that of AIVL—driven almost entirely by a striking 4.77% contribution from share count reduction. This isn't incidental; it's by design. WTV is explicitly built to identify companies that return capital through dividends and share buybacks, and it rewards firms with consistent and high-quality capital return programs. That focus translates into a portfolio that structurally tilts toward shareholder-friendly behavior—a key ingredient in its historical outperformance.

AIVL, on the other hand, doesn't chase shareholder yield as an input. It allows its AI model to assess and rank companies across a vast feature set, of which capital return is only one option. As a result, AIVL's profile closely mirrors that of the Russell 1000 Value Index, which also doesn't screen for capital return behavior. This is what makes WTV unique in the value space: it's not just searching for "cheap" stocks—it's searching for companies that are actively rewarding their shareholders in tangible, recurring ways. And in a market where fundamentals and discipline are regaining importance, that design choice may prove increasingly consequential.

Sources: WisdomTree, FactSet, with data as of 3/30/25. Subject to change. For definitions of terms in the chart above, please visit the glossary.

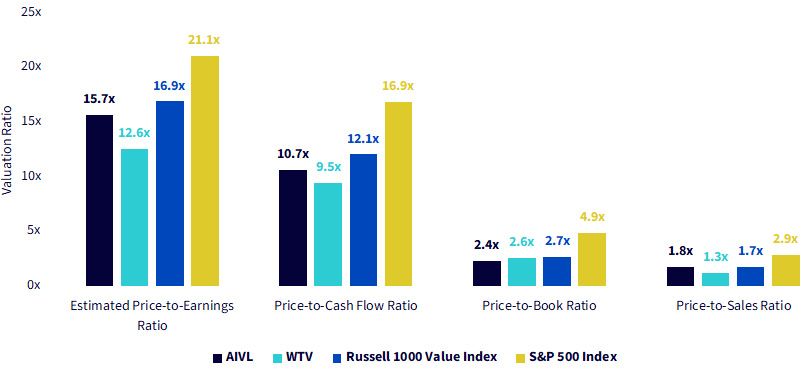

One of the more surprising—but powerful—revelations in figure 5 is WTV's position on estimated price-to-earnings (P/E). At 12.6x, it's the lowest multiple among all four strategies and benchmarks, including the Russell 1000 Value Index. That's remarkable for a Fund with strong recent performance. It suggests that WTV hasn't had to "pay up" for returns—it's finding success by leaning into companies that are both profitable and attractively valued. For investors who still begin their valuation analysis with the P/E ratio, this is a standout differentiator.

What's also notable is how tightly clustered the other valuation metrics are across AIVL, WTV and the Russell 1000 Value Index. On price-to-book, price-to-sales and price-to-cash-flow, the differences are relatively muted—underscoring that WTV's edge is not about extreme valuation compression across the board, but about being meaningfully cheaper where it counts. In a world where even many "value" portfolios can quietly drift up the multiple curve, WTV shows that disciplined selection rooted in capital return and fundamental strength can still lead to an attractively priced portfolio.

Sources: WisdomTree, FactSet, with data as of 3/30/25. Subject to change.

In a market that continues to challenge traditional definitions, the conversation around value investing has never been more important—or more interesting. What we've seen in the comparison between WTV and AIVL, it is not a matter of right or wrong, but rather a clear demonstration that how you define value—and how you implement it—shapes everything. AIVL reflects a cutting-edge, adaptive approach, leaning on artificial intelligence to parse vast data and adjust to regime shifts. It aligns closely with benchmark behavior and offers a model of modern, systematic investing that seeks to stay in tune with evolving signals.

WTV, in contrast, represents a bold, high-conviction stance: value as capital returned to shareholders. Its screens reward discipline—dividends and buybacks—while rigorously filtering out value traps. The result is a portfolio with significantly lower valuations, dramatically higher shareholder yield and—critically—a track record of performance that has not only kept up with the market, but often outpaced it. WTV isn't trying to be all things to all investors. It's designed with purpose, and that purpose is showing up clearly in the numbers.

In a landscape full of smart models and passive tilts, WTV reminds us that, sometimes, value investing still works best when you know exactly what you're looking for. Whether investors favor the interpretive power of AI or the simplicity of cash flow discipline, what matters is choosing a strategy whose construction aligns with their conviction.

1 Source: M.J. Wilson, et al., "U.S. Equities Mid-Year Outlook: Focus on Rate of Change," Morgan Stanley Research, 5/21/25.

2 Source: Wilson et al., 2025.

3 Source: Wilson et al., 2025.

4 Source: Wilson et al., 2025.

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. While the Funds are actively managed, the Funds’ investment process is expected to be heavily dependent on quantitative models and the models may not perform as intended. Please read the Funds’ prospectus for specific details regarding the Funds’ risk profile.

AI Model Risk: When Models and Data prove to be incorrect or incomplete, any decisions made in reliance thereon may lead to the inclusion or exclusion of securities that would have been excluded or included had the Models and Data been correct and complete. Errors in the Models and Data, calculations and/or the construction of the AI model may occur from time to time and may not be identified and/or corrected by the Sub-Adviser or other applicable party for a period of time or at all, which may have an adverse impact on the Fund and its shareholders.

Value Investing Risk: Value stocks, as a group, may be out of favor with the market and underperform growth stocks or the overall equity market, in addition value stocks may not realize their perceived intrinsic value for extended periods of time or may never realize their perceived intrinsic value.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.