GCC

Enhanced Commodity Strategy Fund

Published February 27, 2025

Picture this: it's 2025, and the world is still grappling with fragile supply chains, inflation that refuses to ease and geopolitical tensions that keep redrawing the map of global trade. In times like these, one asset class—often overshadowed in tech-driven bull markets—has stepped back into the spotlight: commodities.

Think of commodities not just as raw materials, but as the pulse of the global economy. The race for green energy has put an unprecedented squeeze on critical metals, making supply chains for lithium, copper and rare earths geopolitical chess pieces. Agricultural commodities have taken center stage as food security becomes a pressing concern for governments worldwide. And oil and gas? They're as unpredictable as ever, caught between economic pragmatism and climate ambitions.

For investors, this isn't just another cyclical trade. Commodities offer something different—seeking a hedge against inflation, a play on real assets and a way to gain exposure to some of the most powerful macro forces reshaping markets. With equity valuations hovering near historical highs and bond markets adjusting to shifting rate expectations, the case for commodities in portfolios has never been more compelling.

There will be tariffs and the threat of tariffs. Importantly, the Trump Administration has already declared an emergency at the Southern border allowing tariffs to be implemented through the International Emergency Economic Powers Act. This does not require Congress and allows the Executive branch to place tariffs as it sees fit. While some actions have been announced and delayed (Mexico and Canada) or cancelled (Colombia), others have been implemented (China). The announcement of reciprocal tariffs is important due to its near blanket applicability. Instead of attempting to front-run or predict the policy shifts and targets, it is worthwhile to step back and understand that tariffs will continue to be a tool of negotiation for the White House. Tariffs and the threat of tariffs are going to continue. There are few knowns around the trajectory of trade policy, but one is that "policy volatility" will persist.

There are many ways these policies filter into the commodity complex. Placing or threatening tariffs across certain commodity products—including crude steel and aluminum—has caused prices to fluctuate meaningfully. This will cause various disruptions and opportunities for investors, requiring nimbleness and thoughtfulness as the headlines flow through markets.

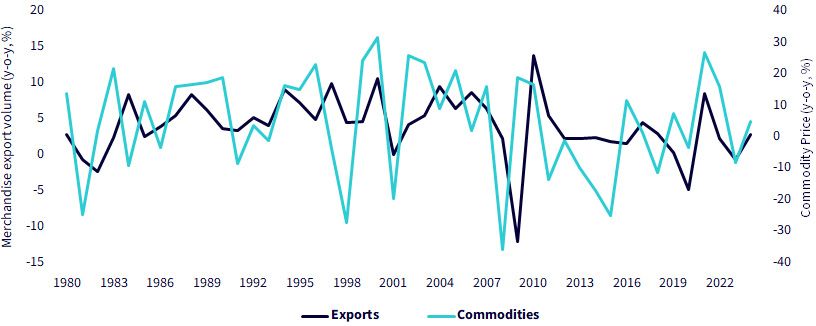

In figure 1, growth in commodity prices and growth in global exports volumes from 1980 to 2024 are displayed over each other. Figure 1 indicates that export weakness is usually coupled with commodity price weakness.

Sources: WisdomTree, Bloomberg. Commodity is Bloomberg Commodity Index Total Return. Past performance is not indicative of future results. You cannot directly invest in an index.

We believe there is significant potential for tariffs and trade frictions to be less severe than what is currently priced into commodity markets. However, for now, the uncertainty remains a downside risk for the broader commodity complex.

Tariffs could contribute to higher inflation in the U.S. while simultaneously depressing global commodity prices due to demand destruction. This dynamic could complicate the Federal Reserve's efforts to manage inflation, potentially leading to U.S. policy interest rates remaining elevated for a longer period.

Geopolitical risk remains top-of-mind for many investors. The past five years have seen a pandemic, the Russian invasion of Ukraine and a war between Israel and Hamas. But geopolitical risk is not static. It changes and shifts rather quickly. The pandemic saw oil prices briefly go negative in the U.S., only to have oil prices surge back over $100 following the invasion of Ukraine and remain steady during the Israel-Hamas conflict. That is all in the past, and the relevant question is how the geopolitical landscape evolves.

Recently, there has been a steady decline in incremental geopolitical risk. Hamas and Israel agreed to a ceasefire. While the ceasefire is fragile, it is a signal of willingness to come to an agreement on both sides to end the current conflict. President Trump then announced conversations with Russian President Putin and Ukrainian President Zelensky to attempt to bring a détente to that conflict. That is not straightforward, and any agreement will take time. But it is—again—a signal of willingness. Both of these developments reduce the level of geopolitical risk in the system, easing the geopolitical price premium in oil, natural gas and gold.

Trump has also voiced disappointment over the European Union's insufficient purchase of U.S. natural gas. If Trump succeeds in ending the Russia-Ukraine war, U.S. sanctions on Russia would likely ease. This raises the question of whether Europe would follow suit. An end to the war could weaken the U.S.'s ability to pressure the EU into buying more American oil and gas, as Russia's gas supplies would become more readily available. Iranian sanctions will escalate under the new Administration. This could drive oil prices higher, encouraging OPEC members to offset this impact by increasing their supply—either explicitly or through non-compliance with production quotas.

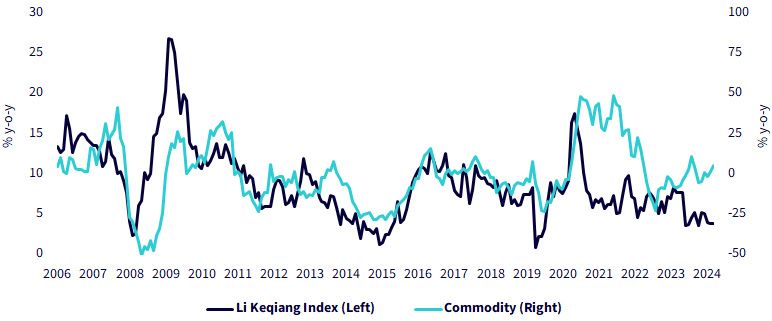

China, as the world's largest consumer of commodities, has cast a shadow over the commodity complex with its relatively poor economic performance in recent years. However, as figure 2 shows, commodities have still managed to perform well despite these challenges.

In previous economic cycles, China was quick to implement grand stimulus measures to boost demand, often through large-scale, commodity-intensive infrastructure and real estate projects. This time, however, the government and central bank have taken a far more measured approach, opting for piecemeal, micro-targeted stimulus initiatives.

While the government has managed to prevent a complete collapse of the real estate sector, the situation remains far from a meaningful recovery.

In figure 2, growth in commodity prices and a measure of Chinese economic growth from 2006 60 2024 are displayed over each other. Figure 2 indicates that Chinese economic weakness is usually coupled with commodity price weakness.

Sources: WisdomTree, Bloomberg. January 2005–December 2024. Li Keqiang index: 40% outstanding bank loans, 40% electricity production, 20% rail freight volume. Commodity is Bloomberg Commodity Index Total Return. Past performance is not indicative of future results. You cannot directly invest in an index.

The Chinese government acknowledges the country's slower population growth and more mature economic stage, which are likely to cap housing demand. As a result, it is wary of triggering new real estate investment bubbles. Indebtedness is another key concern, particularly as local government debts have become more visible following their transfer to central government accounts through various debt swap arrangements.

In recent years, China has accelerated its net-zero emissions ambitions, investing heavily in the infrastructure needed for a clean-tech future. This focus has supported metal prices in the absence of significant demand growth from the real estate sector. We expect this approach to continue, given China's dominance in solar, battery and electric vehicle technology production. Potential U.S. tariffs could push China to further promote domestic adoption of these technologies, moving the country closer to energy independence.

If tensions escalate into a tit-for-tat trade war, China may impose additional export restrictions on critical materials. For example, in 2023, China restricted exports of gallium, germanium and graphite to the U.S., followed by antimony and superhard materials in 2024. While these measures were primarily responses to semiconductor trade disputes, similar restrictions could be applied to energy transition materials.

China's policy efforts are complicated by a depreciating yuan. The People's Bank of China (PBoC) manages the currency by setting a central reference point with a positive or negative 2% fluctuation range. To maintain stability, the PBoC has had to intervene heavily, which limits its capacity to lower interest rates. In September 2024, the government announced a pivot to boost growth, leading to an initial surge in Chinese equity markets and commodities. However, further action has been limited, likely constrained by ongoing currency pressures.

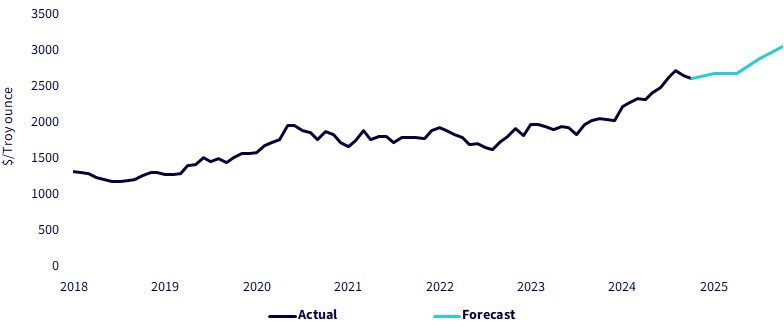

Gold was the best-performing metal of 2024, gaining 27% and reaching a new all-time high of $2,789/oz in October 2024. We believe gold will surpass $3,000/oz this year, even if the U.S. dollar remains strong, and bond yields stay elevated. However, if the U.S. dollar weakens and bond yields decline slightly, as consensus estimates suggest, gold could rise even further, potentially reaching $3,070/oz (as shown in figure 3). Notably, gold has managed to defy the twin headwinds of a strong dollar and high bond yields over the past few months.

Figure 3 shows historical gold prices from 2012 to 2024 and then WisdomTree's forecast to end 2025 in $/troy ounce.

Sources: WisdomTree Model Forecasts, Bloomberg Historical Data, data available as of December 2024. Past performance is not indicative of future results.

Gold is widely viewed as a hedge against financial market turbulence. In December 2024 and early January 2025, equity markets experienced some volatility following the initial strong rally after Trump's election in November 2024. However, by the end of January, equity markets had recovered most of their losses.

The Israel-Hamas ceasefire and a potential resolution to the Ukraine-Russia war could pose risks to the geopolitical premium in gold. However, we believe these geopolitical concerns could easily be replaced by others, such as a marginalized Iran behaving more unpredictably.

Central bank demand for gold remains robust. Notably, the PBoC resumed gold purchases in November and December 2024 after a pause since May 2024. This reinforces our confidence that China remains committed to its currency diversification strategy, with gold serving as a primary tool for seeking diversification.

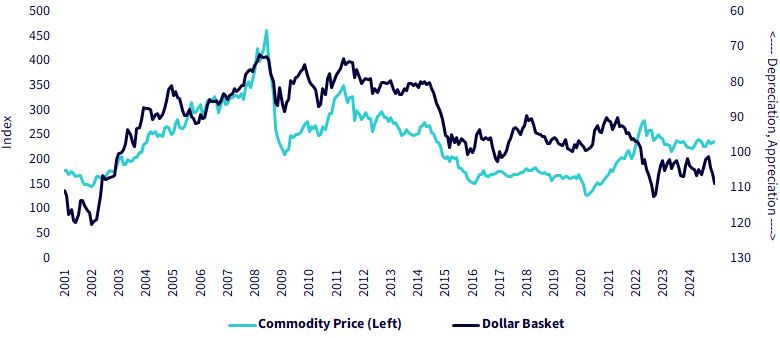

Historically, a strong U.S. dollar has been linked to weaker commodity prices. While this relationship has not always held true in the post-COVID era, the recent resurgence of dollar strength could once again put pressure on commodities.

In figure 4, the returns of a commodity price index and a dollar price index from 2001 to 2024 are displayed over each other. Figure 4 indicates that dollar strength is usually coupled with commodity price weakness.

Sources: WisdomTree, Bloomberg, 2001–2004. Commodity is Bloomberg Commodity Index Total Return. Past performance is not indicative of future results.

As policies become clearer, we may find that our fears were overstated, potentially paving the way for a relief rally across the broader commodity complex. Additionally, it can be challenging to attempt to choose individual commodities, as they can be quite volatile.

The WisdomTree Enhanced Commodity Strategy Fund (GCC) represents a broad basket of commodities and intends to provide broad-based exposure, primarily through investments in futures contracts, to the following four commodity sectors: energy, agriculture, industrial metals and precious metals. The Fund may also invest up to 10% of its net assets in any combination of shares of one or more exchange-traded products that primarily hold bitcoin and in bitcoin futures contracts. The Fund will not invest in bitcoin directly. The Fund will not invest directly in physical commodities.

Commodity investors have familiarity with the following benchmarks:

Translating this into a tangible takeaway for investors: The S&P GSCI Index is well-known for having a particularly heavy exposure to oil. Many of us remember how the price of oil plummeted during the heart of the Covid-19 pandemic in March and April 2020—and this price has since recovered to more normal levels. There are times when oil dominates the commodity story…and there are times when it sits more in the background.

GCC's underlying commodity exposures, historically, look a lot more similar to those of the Bloomberg Commodity Index than those of the S&P GSCI Index. GCC is also seeking to be a bit forward-looking by including an exposure to bitcoin, which neither the S&P GSCI Index nor the Bloomberg Commodity Index currently include. Bitcoin's price can also generate rather extreme volatility in both directions—and this can be an important factor in explaining GCC's performance relative to these benchmarks.

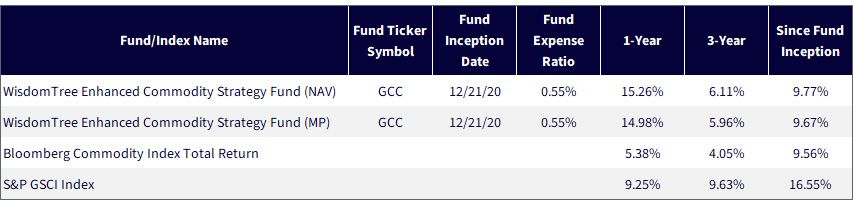

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 2/13/25 with returns as of 12/31/24. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

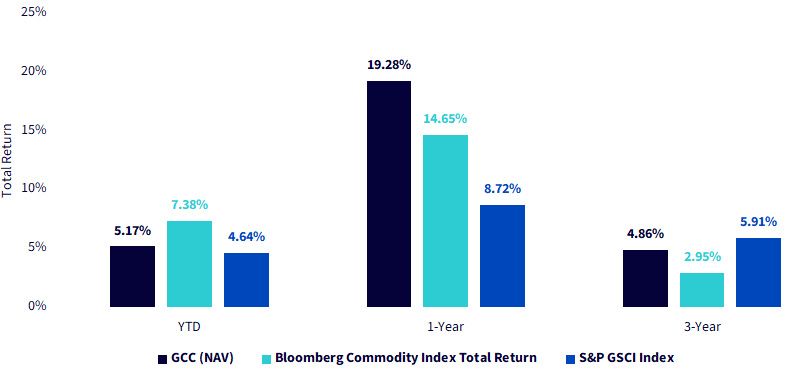

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 2/13/25, with returns as of 2/12/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

As people look at the current backdrop and consider a commodity exposure, we believe that GCC's track record indicates the capacity to be a bit forward looking, including new things like bitcoin at the forefront rather than waiting for the broader market.

There are risks associated with investing, including the possible loss of principal. An investment in this Fund is speculative, involves a substantial degree of risk, and should not constitute an investor’s entire portfolio. One of the risks associated with the Fund is the complexity of the different factors that contribute to the Fund’s performance. These factors include use of commodity futures contracts. In addition, bitcoin and bitcoin futures are a relatively new asset class. They are subject to unique and substantial risks, and historically, have been subject to significant price volatility. While the bitcoin futures market has grown substantially since bitcoin futures commenced trading, there can be no assurance that this growth will continue. In addition, derivatives can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions. The value of the shares of the Fund relate directly to the value of the futures contracts and other assets held by the Fund and any fluctuation in the value of these assets could adversely affect an investment in the Fund’s shares. Because of the frequency with which the Fund expects to roll futures contracts, the price of futures contracts further from expiration may be higher (a condition known as “contango”) or lower (a condition known as “backwardation”) and the impact of such contango or backwardation may be greater than the impact would be if the Fund experienced less portfolio turnover. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Enhanced Commodity Strategy Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.