GCC

Enhanced Commodity Strategy Fund

Published April 9, 2026

Global Head of Research

At the time of this writing, a two-week ceasefire has been on the table. While we are hopeful it can hold, we recognize that there is still importance in understanding different commodity linkages and recognizing certain paths to recovery could be longer than others.

Even if the two week ceasefire agreement leads into a medium or longer-run cessation of hostilities, with or without a toll for passage in the Strait of Hormuz, flows of goods through this passage may not quickly return to normal. The conflict has already caused meaningful damage to production and export infrastructure. In several cases, that damage will take months or even years to repair.

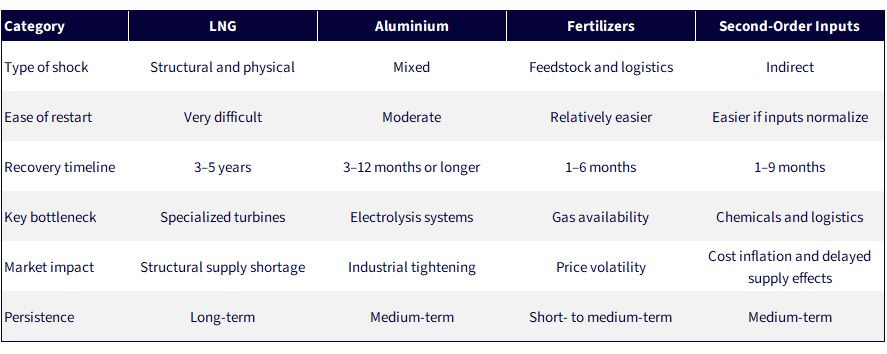

The key point is that geopolitical de-escalation does not immediately translate into supply normalization. The sections below examine how this may play out across energy, industrial metals and fertilizers, before turning to the less visible but equally important second-order effects.

Among all commodities, LNG stands out as the most severely affected. The damage is highly concentrated, but it is concentrated in the most critical part of the global system: Qatar’s Ras Laffan complex.

Strikes on liquefaction trains have resulted in a meaningful loss of capacity, estimated at around 17%, equivalent to roughly 12–13 million tons per annum. At the peak of disruption, this translated into close to one-fifth of global LNG supply being affected. Force majeure declarations underline the severity of the situation.1

Additional disruption has occurred upstream, particularly in Iran’s South Pars gas field, as well as across a wider set of regional energy assets. In total, more than 40 energy sites across multiple countries have reportedly been damaged, with repair costs already exceeding $25 billion.2

What distinguishes LNG from other sectors is the nature of the bottleneck. Liquefaction facilities depend on highly specialized turbines with limited global manufacturing capacity and long lead times. This makes any recovery structurally slow.

Source: Martinsen, A., Satwani, K., & Selvaraju, K. (2026, March 25). The cost of war: Gulf energy infrastructure left facing a $25 billion repair bill. Rystad Energy.

Even in a scenario where hostilities subside quickly, LNG markets are likely to remain tight for several years due to these structural constraints.

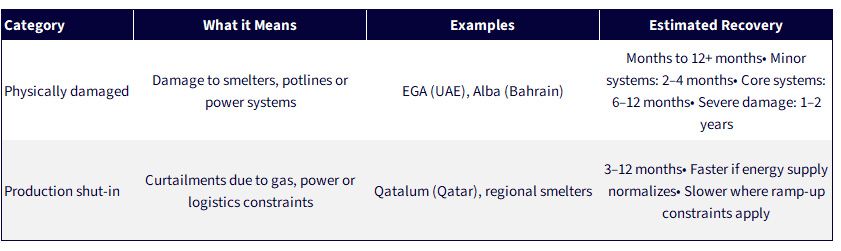

The aluminum sector presents a more complex picture. Unlike LNG, where the disruption is concentrated and structural, aluminum is affected through a combination of direct damage and indirect constraints.

There is confirmed physical damage at major Gulf smelters, alongside production curtailments driven by disruptions to gas supply and logistics. Facilities in the UAE and Bahrain have reported damage, while operations in Qatar have been scaled back due to feedgas constraints.3

The situation at Qatalum provides a useful reference point. A controlled shutdown was initiated when gas supply was disrupted, and although operations have partially resumed, output remains below full capacity. The expected timeline for a full restart is in the range of six to twelve months. This suggests that, in this case, the constraint is primarily related to energy availability rather than irreversible damage to core assets.4

At other sites, where physical damage has occurred, the timeline is more uncertain. Aluminum smelting is a continuous process, and restarting production requires careful management of potlines and electrical systems. Repairs therefore tend to take longer than in many other industrial sectors.

Sources: Norsk Hydro ASA. (2026, March 3). Qatalum initiates controlled shutdown of aluminum production; Financial Times. (2026, March 5). Iran war triggers aluminum supply crunch and shutdowns across Middle East.

Overall, aluminum is likely to recover more quickly than LNG, but not immediately. The combination of physical repair requirements and operational constraints means that supply will remain below normal levels for some time.

Fertilizer markets are shaped less by physical destruction and more by disruptions to the system as a whole. Three channels are particularly important.

First, fertilizer production is highly dependent on natural gas, which is the primary feedstock for ammonia. Disruptions to gas supply therefore translate directly into production shut-ins. Second, there has been some physical damage to petrochemical infrastructure, although this appears more limited than in the energy sector. Third, and perhaps most importantly, trade flows have been disrupted by risks to shipping through the Strait of Hormuz.

This combination makes fertilizers highly sensitive to both energy markets and logistics.

Sources: Ewing, R. (2026, March 20). Ammonia prices firm on Middle East supply shock, though new US capacity cushions impact in West. Profercy; Gordon, N., & Corthell, L. (2026, March). The other global crisis stemming from the Strait of Hormuz’s blockage. Carnegie Endowment for International Peace.

In contrast to LNG, fertilizer production can resume relatively quickly once gas supply and logistics stabilize. However, this also means that prices are likely to remain volatile, responding rapidly to changes in underlying conditions.

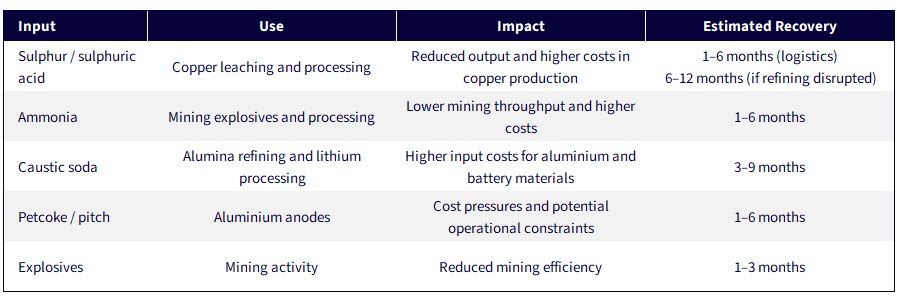

Beyond the direct impact on energy and industrial production, the Middle East plays a crucial role in supplying chemical inputs used across the metals and mining sectors. Disruptions in these inputs create second-order effects that are less visible initially but can become significant over time.

These inputs include sulphur, ammonia and various petrochemical derivatives, all of which are essential to different stages of metal production.

Sources: S&P Global Commodity Insights. (2026, March). Commodity market disruptions across energy, metals, and chemicals amid Middle East supply shock; International Copper Study Group. (2025). The world copper factbook 2025.

These effects tend to emerge with a lag. Initially, markets react to the most visible disruptions in energy and trade. Over time, however, constraints in chemical inputs begin to feed through into production costs and, in some cases, output levels.

Source: WisdomTree, summarizing the prior 4 figures as well as facts and figures presented in this piece.

At first glance, the crisis presents itself as a classic energy shock. The most visible disruptions have been in oil and gas markets, and price reactions have been led by LNG and crude.

However, as the analysis above shows, the impact extends well beyond energy.

Disruptions to gas supply feed directly into fertilizer production. Fertilizers, in turn, are closely linked to agricultural markets and food prices. At the same time, constraints in refining and petrochemical activity reduce the availability of key industrial inputs such as Sulphur, ammonia and caustic soda. These inputs are essential to the production of metals including copper, aluminum and battery materials.

What begins as an energy shock therefore propagates through multiple layers of the global economy:

For investors, this has important implications.

Focusing solely on oil and gas may capture the initial phase of the shock, but it risks missing the broader and more persistent effects that emerge over time. As supply constraints ripple through interconnected markets, a wider set of commodities becomes exposed.

A more resilient approach is therefore to consider broad commodity exposure, rather than concentrating only on energy. This allows investors to participate not just in the immediate price response, but also in the second-order effects that tend to unfold with a lag.

In that context, diversified commodity strategies can provide a more comprehensive way to navigate periods where geopolitical disruption affects multiple parts of the supply chain simultaneously.

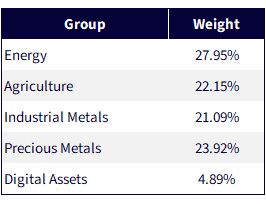

The WisdomTree Enhanced Commodity Strategy Fund (GCC) is an example of such a broad-based commodity strategy. In evaluating broad commodity strategies, we think one of the most important under-the-hood considerations is exposure to energy. This is not to say there is a ‘good’ or ‘bad’ level, but rather important considerations if diversification and broad exposure are the most important underlying drivers of a commodity thesis. A large exposure to energy, in our view, could reduce the diversification of a more broadly-exposed strategy. Figure 6 shows the broad commodity group exposures of GCC as of March 31, 2026. Of course, these are subject to change over time.

Source: WisdomTree, specifically GCC’s fund page, with data as of 3/31/2026. Subject to change.

Al-Kaabi, S. S. (March 19, 2026). Iranian attacks knock out 17% of Qatar’s LNG capacity, with 12.8 million tonnes per year offline and force majeure declared on long-term contracts [Interview]. Reuters.

Birol, F. (March 23, 2026). Remarks on Middle East energy infrastructure damage at the National Press Club, Canberra (reported by Bloomberg). bne IntelliNews; Martinsen, A., Satwani, K., & Selvaraju, K. (March 25, 2026). The cost of war: Gulf energy infrastructure left facing a $25 billion repair bill. Rystad Energy.

Burton, M. (April 1, 2026). Top Gulf aluminum producer halts smelter after Iran strike. Bloomberg News.

Norsk Hydro ASA. (March 3, 2026). Qatalum initiates controlled shutdown of aluminum production.

There are risks associated with investing including possible loss of principal. An investment in this Fund is speculative, involves a substantial degree of risk, and should not constitute an investor's entire portfolio. One of the risks associated with the Fund is the complexity of the different factors which contribute to the Fund's performance. These factors include use of commodity futures contracts. In addition, bitcoin exchange-traded products (ETPs) and bitcoin futures are relatively new and the markets may be less developed. They are subject to unique and substantial risks, and historically, have been subject to significant price volatility. As a result, the markets for bitcoin futures and bitcoin ETPs may be less developed, and at times, potentially less liquid and more volatile, than more established commodity futures and ETP markets. While the bitcoin futures market has grown substantially since bitcoin futures commenced trading, there can be no assurance that this growth will continue. In addition, derivatives can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions. The value of the shares of the Fund relate directly to the value of the futures contracts and other assets held by the Fund and any fluctuation in the value of these assets could adversely affect an investment in the Fund's shares. Because of the frequency with which the Fund expects to roll futures contracts, the price of futures contracts further from expiration may be higher (a condition known as “contango”) or lower (a condition known as “backwardation”) and the impact of such contango or backwardation may be greater than the impact would be if the Fund experienced less portfolio turnover. The Fund will not invest in bitcoin directly. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Enhanced Commodity Strategy Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.