The Appeal of Agency Mortgage-Backed Securities in a Shifting Economic Landscape

Published September 19, 2024

Behnood Noei, CFA

Director, Fixed Income

Andrew Okrongly, CFA

Director, Model Portfolios

Key Takeaways

- With the Fed moving into a rate-cutting cycle, many investors are thinking about how to move from cash into longer-duration fixed income investments.

- Within our fixed income Model Portfolios, we have been extending duration over the past several years and are now roughly neutral to our benchmark.

- A sector that could stand to benefit from lower interest rates is agency mortgage-backed securities.

- While the sector offers compelling valuations, all mortgages are not created equal, and investors need to be mindful of the risks inherent in current coupon mortgages.

This article is relevant to financial professionals who are considering offering model portfolios to their clients. If you are an individual investor interested in WisdomTree ETF Model Portfolios, please inquire with your financial professional. Not all financial professionals have access to these Model Portfolios.

Following the September FOMC meeting where the Federal Reserve kicked off a new easing cycle, inflation continues to moderate and economic data shows signs of slowing.

For fixed income investors who have adopted the “t-bill and chill” mantra, this could serve as a wake-up call that the days of earning greater than 5% yield with no volatility are coming to an end.

We expect that the attention of many such investors will soon shift (or perhaps already has) toward reinvestment risk.

Indeed, it was our expectation for monetary policy normalization that led our Model Portfolio Investment Committee to gradually move to a neutral duration position throughout last year.

A challenge facing investors looking further out on the yield curve is that investment-grade corporate bonds, and the core bond strategies that hold them, don’t appear particularly attractive at the moment.

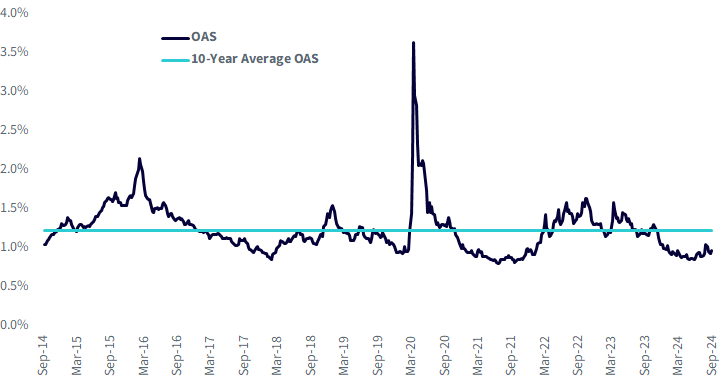

Figure 1: Credit Spreads (OAS) on Investment-Grade Corporate Bonds Remain below Long-Term Averages

Sources: WisdomTree, FactSet, as of 9/5/24. Represented by the OAS of the Bloomberg US Corporate Bond Index. You cannot invest

directly in an index. Past performance is not indicative of future returns.

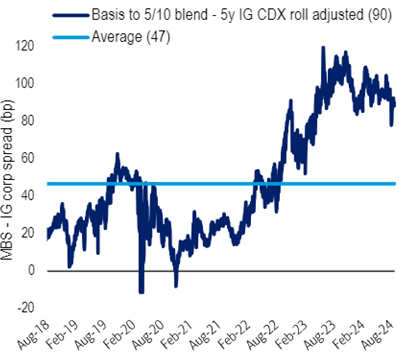

One area of the fixed income landscape that does currently offer a historically attractive yield premium is agency mortgage-backed securities (agency MBS).

One of the largest asset classes in the U.S. bond market, the principal and interest of agency MBS are guaranteed by government-sponsored entities (GSEs) such as Fannie Mae, Freddie Mac and Ginnie Mae, which benefit from their relationship with the U.S. government.

Even with this implicit backing, an MBS typically provides a yield premium (measured by option-adjusted spread, or OAS) compared to Treasuries as compensation for investors assuming the prepayment risk embedded in the underlying mortgages.

This spread is currently well above its own long-term average and at a significant historical premium to corporate bonds.

Figure 2: Agency MBS Yield Premium Relative to Investment-Grade Corporate Bonds

Source: BofA Global Research, as of 9/5/24. Yield premium represented by

the MBS basis and 5y IG CDX spread. You cannot invest directly in an index.

Past performance is not indicative of future returns.

In addition to attractive valuations, agency MBS has been one of the top-performing fixed income sectors since the start of the third quarter, up more than 8% in less than three months.1 Driven by a combination of rate and spread moves, we believe this recent performance is largely explained by investor rotation into high-quality, longer-duration asset classes as the economy starts to slow and the Fed prepares to cut rates.

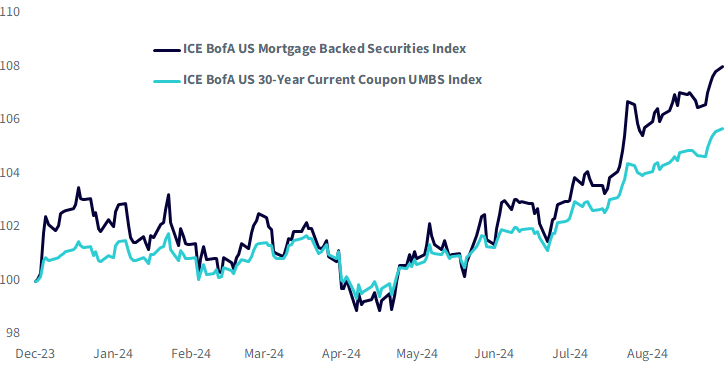

However, as outlined in one of our previous posts back in December 2023, not all agency mortgages are created equal.

Strategies targeting higher-yielding current coupon mortgages have gathered significant assets in recent quarters. As reiterated in that post, one of the biggest risks associated with current coupon mortgages is their more negative convex nature. This can be seen in the difference between the performance of a broad-based agency MBS index and a 30-year current coupon equivalent. Since writing that post on December 11, 2023, current coupon mortgages have underperformed the broad index by roughly 225 basis points.

Figure 3: Recent Performance of Current Coupon Mortgages vs. the Broad Agency MBS Index

Source: ICE, as of 9/9/24. Past performance is not indicative of future results. You cannot directly invest in an index.

In summary, we believe agency MBS remains an attractive option for investors looking to lock in yields and extend duration into high-quality fixed income ahead of the upcoming Fed rate cut cycle.

However, agency mortgages are a nuanced asset class, and investors should be fully aware of the risks involved in strategies that target single cohorts of the sector with the allure of higher yields.

In our Model Portfolios, which have an over-weight to securitized assets and agency MBS, we typically allocate to broad, actively managed strategies that can diversify exposures across coupons, manage convexity risk and capitalize on specific opportunities when they arise.

Financial advisors can learn more about the WisdomTree CIO Managed lineup of fixed income and multi-asset Model Portfolios by visiting our Portfolio Solutions offerings.

1 Source: ICE, as of 9/9/24.

Important Risks Related to this Article

For financial advisors: WisdomTree Model Portfolio information is designed to be used by financial advisors solely as an educational resource, along with other potential resources advisors may consider, in providing services to their end clients. WisdomTree’s Model Portfolios and related content are for information only and are not intended to provide, and should not be relied on for, tax, legal, accounting, investment or financial planning advice by WisdomTree, nor should any WisdomTree Model Portfolio information be considered or relied upon as investment advice or as a recommendation from WisdomTree, including regarding the use or suitability of any WisdomTree Model Portfolio, any particular security or any particular strategy.

For retail investors: WisdomTree’s Model Portfolios are not intended to constitute investment advice or investment recommendations from WisdomTree. Your investment advisor may or may not implement WisdomTree’s Model Portfolios in your account. The performance of your account may differ from the performance shown for a variety of reasons, including but not limited to: your investment advisor, and not WisdomTree, is responsible for implementing trades in the accounts; differences in market conditions; client-imposed investment restrictions; the timing of client investments and withdrawals; fees payable; and/or other factors. WisdomTree is not responsible for determining the suitability or appropriateness of a strategy based on WisdomTree’s Model Portfolios. WisdomTree does not have investment discretion and does not place trade orders for your account. This material has been created by WisdomTree, and the information included herein has not been verified by your investment advisor and may differ from information provided by your investment advisor. WisdomTree does not undertake to provide impartial investment advice or give advice in a fiduciary capacity. Further, WisdomTree receives revenue in the form of advisory fees for our exchange-traded Funds and management fees for our collective investment trusts.

About the contributors

Behnood Noei, CFA

Director, Fixed Income

Behnood Noei serves as Director of Fixed Income at WisdomTree Asset Management, where he develops the firm’s suite of fixed income and currency exchange-traded funds and enhances existing investment processes. Behnood has 11 years investment experience in portfolio management and quantitative research. Prior to joining WisdomTree in 2022, Behnood was a portfolio manager and developer of some of the fixed income ETFs at J.P.Morgan Asset Management, where he was directly responsible for managing more than 7 Fixed Income ETFs and multiple SMAs with more than $13Billion in assets. He graduated from The Ohio State University with Master of Science degree in Finance and is a CFA charter holder.

Andrew Okrongly, CFA

Director, Model Portfolios

Andrew Okrongly joined WisdomTree in 2022 as a Director on the Model Portfolios Team. He is responsible for the design and ongoing management of model portfolios and custom solutions for portfolio managers and advisors. Andrew is also a member of the Model Portfolio Investment Committee. Prior to joining WisdomTree, Andrew was a Director on the Outsourced Chief Investment Officer (OCIO) team at Commonfund, where he was responsible for macro-economic analysis and advising institutional clients on strategic and tactical asset allocation. Andrew began his career at BlackRock where he held a variety of fixed income and multi-asset investment roles. Andrew received a BBA degree from the University of Michigan and is a holder of the Chartered Financial Analyst designation.