DXJ

Japan Hedged Equity Fund

Published August 20, 2025

Director, Fixed Income

Associate, Investment Strategy

Director, Model Portfolios

The big move in Japanese bond yields in the last few weeks raised some inquiries about what it all means for the opportunities in the Japanese equity markets. Our take is that the bull case remains, but let's review the news.

Most attention centered on political uncertainty and a surprise U.S.-Japan trade agreement. Prime Minister Ishiba's position came under scrutiny after his ruling coalition narrowly lost its Upper House majority. While the final seat count wasn't enough to trigger immediate upheaval, the loss stirred speculation about his possible resignation, rumors he quickly denied. Markets seem cautiously optimistic that the government can steer policy by aligning with independents and friendly opposition groups, dialing back earlier fiscal fears.

The announcement of a U.S.-Japan trade deal also caught many off guard and brought a degree of relief. The agreement reduces tariffs on automobiles and parts, although steep duties on Japanese steel and aluminum exports remain in place for now.

BoJ Deputy Governor Uchida called the deal "a very big step forward," suggesting it improves the odds of the central bank hitting its economic targets.

Although another rate hike isn't expected just yet, the path toward policy normalization appears a bit clearer. This drove a flattening in the JGB yield curve, reflecting both higher expectations for BoJ action and a slight easing of long-term fiscal concerns.

Despite the ruling coalition's electoral setback, the overall fiscal outlook hasn't shifted dramatically, particularly if this fall's supplementary budget mirrors 2024 levels, which could avoid additional bond issuance.

While June data revealed sustained strong demand for JGBs from overseas investors, domestic interest remained subdued, as a recent auction for 40-Year JGBs had the lowest bid-to-cover ratio since 2011. Ripple effects spread to the 10-Year tenor, which elevated its yield to 1.6%, the highest in 17 years.

By Japanese standards, these yields are lush and should attract both domestic and international investors. While the demand structure for JGBs remains a key topic to watch, we still believe there are more compelling opportunities in Japanese equities.

WisdomTree Models Over-Weight Japan

As noted earlier this year, WisdomTree Model Portfolios remain focused on Japan within developed international equity, as corporate reforms, geopolitical tailwinds and rising domestic demand present a compelling long-term opportunity to our team.

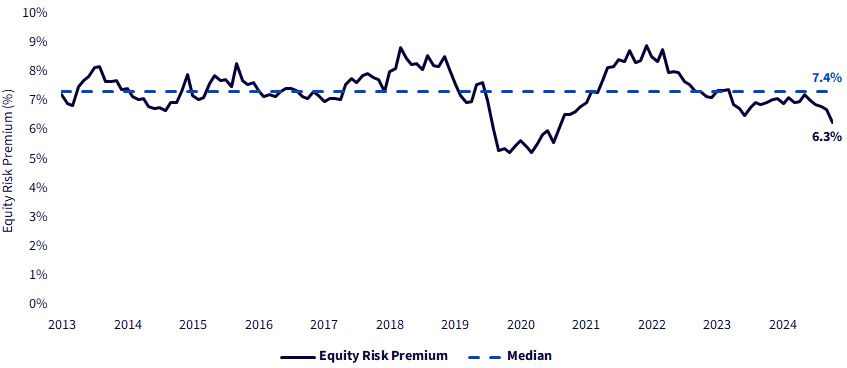

For most of the past 12 years, the Japanese equity risk premium has ranged from 5%–8%. Based on prevailing estimated earnings yields and 10-Year JGB inflation-indexed yields, the current spread is 6.7%. While the JGB yields have hit the highest level, there are still negative inflation-indexed bond yields.

Figure 1: Japan Equity Risk Premium (MSCI Japan Est. Earnings Yield—10-Year JGB Inflation-Indexed Yield)

Sources: WisdomTree, Bloomberg, MSCI, as of 7/29/25. Past performance does not guarantee future results. You cannot invest directly in an index. Subject to change.

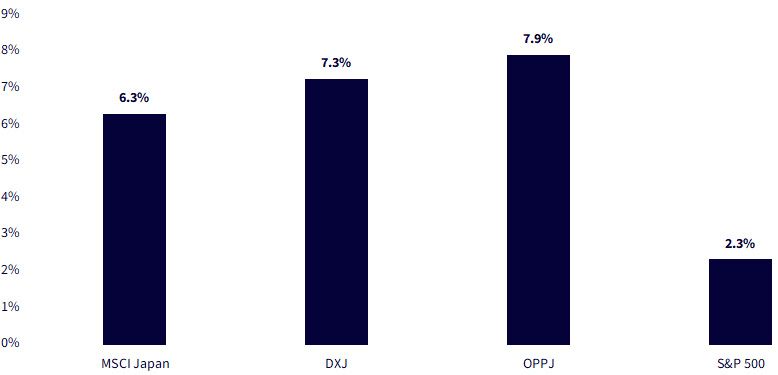

Alternative approaches to Japanese equity investment focused on improving valuations have even higher equity premium spreads.

Figure 2: Current Japan Equity Risk Premiums (Est. Earnings Yield—10-Year JGB Inflation-Indexed Yield)

Sources: WisdomTree, Bloomberg, MSCI, as of 7/29/25. Past performance does not guarantee future results. You cannot invest directly in an index. Subject to change.

Export-oriented stocks, such as those targeted by the WisdomTree Japan Hedged Equity Fund (DXJ), currently supply an additional 1.3% above the market cap-weighted MSCI Japan Index's equity risk premium and currently 8%.

Our new WisdomTree Japan Opportunities Fund (OPPJ)1 takes the equity risk premium analysis a step further due to its focus on even deeper value stocks. It currently offers a forward earnings yield 8.66%greater than that of the 10-Year inflation-indexed JGB.2

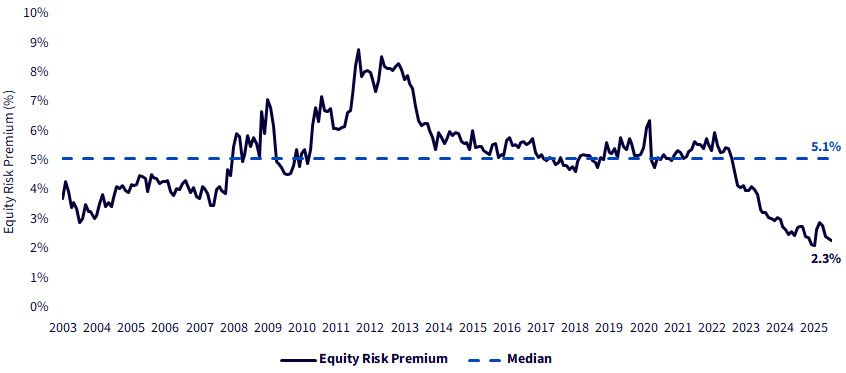

The forward earnings yield on the S&P 500 is only 2.3% greater than the yield currently offered by 10-Year Treasury Inflation-Protected Securities (TIPS), which is nearly 3% below its longer-term median of 5.1%.

With the Japan equity premiums between three and four times that of the S&P 500, we do not think the rise in bond yields provides true competition.

Figure 3: S&P 500 Equity Risk Premium (Est. Earnings Yield—10-Year TIPS Yield)

Sources: WisdomTree, St. Louis Federal Reserve (FRED) database, S&P, as of 7/29/25. Past performance does not guarantee future results. You cannot invest directly in an index. Subject to change.

This implies that, despite the changing dynamics in the equity and bond markets of the U.S. and Japan over the past few years, Japanese equities still offer comparatively attractive earnings yields that may be of service within international equity allocations.

1 Prior to July 1, 2025, the Fund was known as the WisdomTree Japan Hedged SmallCap Equity Fund (DXJS). On that date, the Fund's investment policy changed.

2 Performance is historical and does not guarantee future results. Current performance may be lower or higher than quoted. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance data for the most recent month-end is available click here.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile, and these investments may be less liquid than other securities and more sensitive to the effects of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Director, Fixed Income

Behnood Noei serves as Director of Fixed Income at WisdomTree Asset Management, where he develops the firm’s suite of fixed income and currency exchange-traded funds and enhances existing investment processes. Behnood has 11 years investment experience in portfolio management and quantitative research. Prior to joining WisdomTree in 2022, Behnood was a portfolio manager and developer of some of the fixed income ETFs at J.P.Morgan Asset Management, where he was directly responsible for managing more than 7 Fixed Income ETFs and multiple SMAs with more than $13Billion in assets. He graduated from The Ohio State University with Master of Science degree in Finance and is a CFA charter holder.

Associate, Investment Strategy

Brian Manby joined WisdomTree in October 2018 as an Investment Strategy Analyst. He is responsible for assisting in the creation and analysis of WisdomTree’s model portfolios, as well as helping support the firm’s research efforts. Prior to joining WisdomTree, he worked for FactSet Research Systems, Inc. as a Senior Consultant, where he assisted clients in the creation, maintenance and support of FactSet products in the investment management workflow. Brian received a B.A. as a dual major in Economics and Political Science from the University of Connecticut in 2016. He is holder of the Chartered Financial Analyst designation.

Director, Model Portfolios

Andrew Okrongly joined WisdomTree in 2022 as a Director on the Model Portfolios Team. He is responsible for the design and ongoing management of model portfolios and custom solutions for portfolio managers and advisors. Andrew is also a member of the Model Portfolio Investment Committee. Prior to joining WisdomTree, Andrew was a Director on the Outsourced Chief Investment Officer (OCIO) team at Commonfund, where he was responsible for macro-economic analysis and advising institutional clients on strategic and tactical asset allocation. Andrew began his career at BlackRock where he held a variety of fixed income and multi-asset investment roles. Andrew received a BBA degree from the University of Michigan and is a holder of the Chartered Financial Analyst designation.