GCC

Enhanced Commodity Strategy Fund

Published March 25, 2025

Global Head of Research

There was a time when commodities moved in predictable cycles. Demand would surge, supply would scramble to keep up, and eventually, the cycle would reset. Not anymore. The world isn't waiting for cycles; it's building—everywhere, all at once. Factories, power plants, semiconductor foundries and entire energy grids are being reengineered at a breakneck pace, not just in one country but across multiple industrial powerhouses. Governments, recognizing the urgency of self-reliance, are throwing their weight behind policies that drive infrastructure, manufacturing and energy independence. In this environment, the question isn't whether commodities are entering another cycle; it's whether supply can ever catch up with the sheer scale of what's being built.

In the United States, the economic playbook is shifting again. With a resurgence of Trump-era policies, the focus is squarely on domestic production, supply chain security and energy dominance. Green energy incentives from the previous administration are being reassessed, with fossil fuels once again taking center stage. Expect coal, oil and natural gas to see a resurgence, with deregulation allowing for faster permitting and extraction.1

Meanwhile, the push to reshore critical industries is intensifying. Tariffs on steel, aluminum and key industrial components are being expanded,2 with the explicit goal of reducing reliance on China and other foreign suppliers. The White House's approach to manufacturing isn't just about semiconductors anymore; it's about a full-spectrum industrial revival, from heavy industry to rare earth refining. This isn't a short-term policy; it's a structural shift that will drive demand for raw materials, reshape supply chains and rewrite the global trade order.

Europe's ambitions remain firmly rooted in sustainability, but reality is forcing difficult decisions. The Green Deal Industrial Plan is fueling demand for lithium, nickel and other battery metals,3 yet supply chains remain fragile. Meanwhile, the continent is racing to replace Russian energy imports, driving long-term commitments to liquid natural gas (LNG) infrastructure and nuclear energy. In practice, this means heightened demand for uranium, natural gas and industrial metals, even as policy makers struggle to align environmental goals with economic necessities.

The world isn't just building; it's also protecting what it builds. Trade barriers are becoming the norm, not the exception. The U.S. is doubling down on tariffs, making key metals more expensive on the global market. China is restricting exports of essential battery materials, putting Western automakers in a bind. Europe is crafting new trade agreements to secure access to critical raw materials, bypassing traditional suppliers. In this fragmented trade environment, supply chains are being rewritten in real time, and commodity markets are responding with volatility that isn't going away anytime soon.

Two forces are converging to reshape global energy demand: the green energy transition and the AI-powered digital economy. Governments are mandating aggressive solar, wind and battery storage rollouts, sending demand for critical minerals soaring.4 At the same time, the rise of artificial intelligence and cloud computing is driving an unprecedented electricity surge, fueling investment in natural gas, advanced grid infrastructure and energy storage technologies. Unlike past commodity booms that cooled with economic cycles, this surge in demand is structural—it's the new normal.

For all the world's urgency in building, there's one problem: supply doesn't move at the speed of demand.

With demand rising and supply constrained, investors are positioning themselves accordingly.

The WisdomTree Enhanced Commodity Strategy Fund (GCC) is an actively managed exchange-traded Fund and intends to provide broad-based exposure to the following four commodity sectors: Energy, Agriculture, Industrial Metals and Precious Metals, primarily through investments in futures contracts. The Fund may also invest up to 10% of its net assets in any combination of shares of one or more exchange-traded products that primarily hold bitcoin and in bitcoin futures contracts. The Fund will not invest in bitcoin directly.

In short, a broad-based commodity exposure may help investors position with a recognition that the global infrastructure build we are seeing will require different commodities in different places at different times.

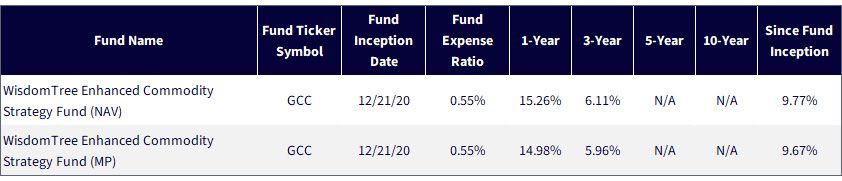

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 3/13/25, with returns as of 12/31/24. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click here.

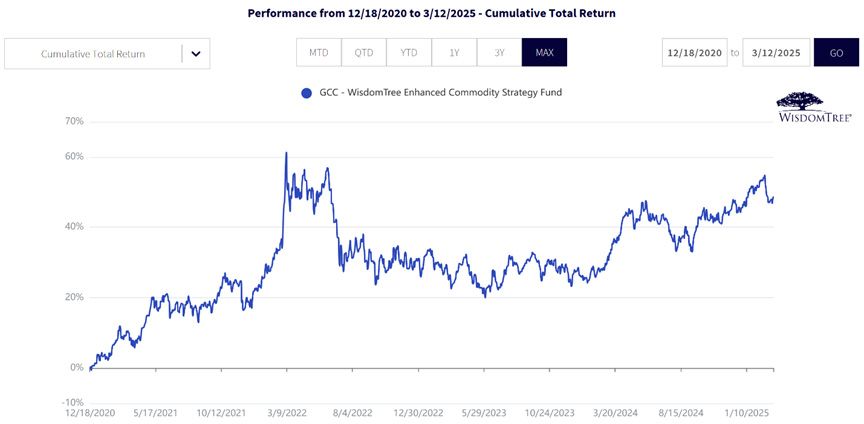

The commodity investment experience in recent years has been dominated by the period of high inflation that directly followed all of the stimulus during the COVID-19 pandemic. We see that GCC hit its historic high quite quickly. After this, there was a period of correction, but we can see in figure 2 that we are starting to get close to that high water mark. We think the focus on building across the global economy could function to push commodities back toward that high water mark and possibly even beyond.

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 3/13/25, with returns as of 3/12/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click here.

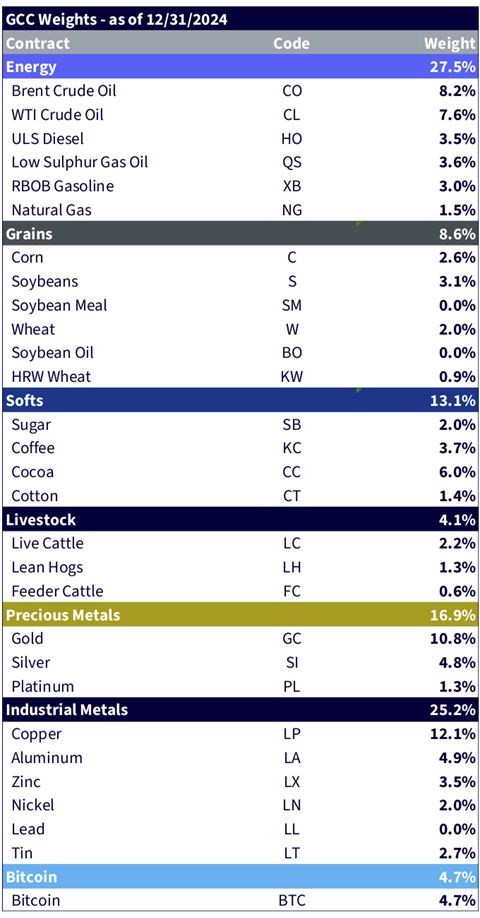

In figure 3, one can appreciate the diversification across more than 25 different commodities within GCC.

Source: WisdomTree. Tin, lead, soybean oil and soybean meal were not selected for inclusion. GCC weights as of 12/31/24. As we rebalance the strategy, actual weights on any business day may vary from rebalance weights due to market price fluctuations. Contract refers to any listed commodity futures contract. Commodity refers to a basic good used in commerce, often used as input in the production of another good or service. The difference between commodity and contract is illustrated through this example: the crude oil commodity is invested in through two different contracts—the WTI Crude (NYMEX) and the Brent Crude (ICE) contracts.

Commodity markets aren't just cycling through another boom—they're transitioning into a structurally different world. Policy makers are no longer reacting to market forces—they're actively shaping them. Governments aren't just incentivizing demand—they're mandating it. Supply chains aren't simply evolving—they're being rewritten by force. The result? A world that is not just consuming more raw materials but is fundamentally changing how, where and why those materials are sourced.

For investors, the opportunities are clear. This isn't about riding a wave—it's about understanding the tectonic shifts underneath the surface. Those who recognize the structural nature of these changes will be best positioned to navigate what comes next.

1 Source: https://www.whitehouse.gov/articles/2025/02/national-energy-dominance-council-paves-way-for-unleashing-american-energy/

2 Source: Ana Swanson & Jeanna Smialek, “Trump’s Tariffs on Steel and Aluminum Go Into Effect, Inciting Global Retaliation,” New York Times, 3/13/25.

3 Source: https://www.iea.org/reports/the-role-of-critical-minerals-in-clean-energy-transitions/executive-summary

4 Source: https://www.reuters.com/business/energy/texas-tops-us-states-renewable-energy-battery-capacity-maguire-2025-01-09/

5 https://press.spglobal.com/2024-07-18-United-States-Ranks-Next-to-Last-in-Development-Time-for-New-Mines-that-Produce-Critical-Minerals-for-Energy-Transition,-S-P-Global-Finds

There are risks associated with investing, including the possible loss of principal. An investment in this Fund is speculative, involves a substantial degree of risk and should not constitute an investor’s entire portfolio. One of the risks associated with the Fund is the complexity of the different factors that contribute to the Fund’s performance. These factors include the use of commodity futures contracts. In addition, bitcoin and bitcoin futures are a relatively new asset class. They are subject to unique and substantial risks and, historically, have been subject to significant price volatility. While the bitcoin futures market has grown substantially since bitcoin futures commenced trading, there can be no assurance that this growth will continue. In addition, derivatives can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions. The value of the shares of the Fund relates directly to the value of the futures contracts and other assets held by the Fund, and any fluctuation in the value of these assets could adversely affect an investment in the Fund’s shares. Because of the frequency with which the Fund expects to roll futures contracts, the price of futures contracts further from expiration may be higher (a condition known as “contango”) or lower (a condition known as “backwardation”), and the impact of such contango or backwardation may be greater than the impact would be if the Fund experienced less portfolio turnover. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Enhanced Commodity Strategy Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.