DXJ

Japan Hedged Equity Fund

Published February 10, 2026

Global Chief Investment Officer

Director, Fixed Income

Rising Japanese bond yields and the weak yen are causing some market consternation as politics and fiscal policy are back in the driver's seat. Initially, Prime Minister Sanae Takaichi dissolved parliament and set a February 8 general election, catching markets off guard, especially with her pledge to scrap a consumption tax on food for two years. The election has delivered a decisive victory for the Liberal Democratic Party under Prime Minister Takaichi, with the ruling bloc securing well above the “absolute stable majority” threshold of 261 seats and exceeding a two-thirds majority in the Lower House. However, there are still questions about the direction of fiscal policy, and longer-dated bond yields have spiked higher.

The rise in yields was large enough that the Bank of Japan commented on the speed of the selloff and suggested it's prepared to step in if trading becomes disorderly, even as it continues to move policy away from ultra-easy settings.

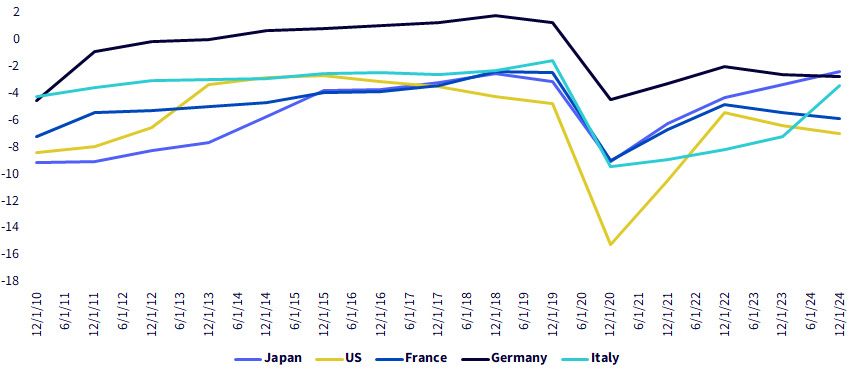

Let's put the recent moves in a better context. Japan's fiscal picture is improving as the economy moves past deflation and nominal growth picks up. Higher nominal gross domestic product (GDP) has translated into stronger tax revenues and a healthier fiscal balance, and the debt-to-GDP ratio has already started to edge lower. If we compare Japan's budget deficit to GDP, it stacks out better than the U.S., France, Italy and Germany—this represents a complete reversal from 15 years ago where it stood as the worst in the group.

It also helps to look at the broader public-sector balance sheet: because the Bank of Japan holds a large share of outstanding long-term JGBs, the headline debt numbers can make the near-term financing situation look worse than it really is.

Source: Bloomberg, WisdomTree, for the period 12/31/10–12/31/24.

Also, where the bond market stress is showing up matters. The biggest swings have been in super-long bonds (20–40 years), a less liquid part of the bond market in which yields can jump even without any real change in Japan's ability to fund itself.

The rise in 10-year yields isn't only about politics or the budget—it is also being driven by Japan moving away from ultra-low rates, the return of inflation at home, and the broader level of interest rates overseas.

Election jitters may keep rates choppy, but we still see more compelling opportunities in Japanese equities.

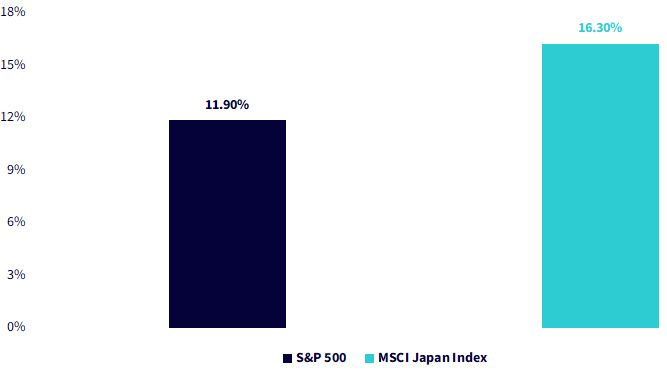

U.S. earnings surged in 2025, supported by continued strength in AI-related technology sectors. Japanese earnings grew even faster. Index-level earnings per share surged late in the year, pushing Japan's cumulative earnings growth well beyond that of the U.S.

Source: WisdomTree, FactSet as of 12/31/25. Forward operating earnings is measured as a combination of actual and estimated earnings. You cannot invest directly in an index.

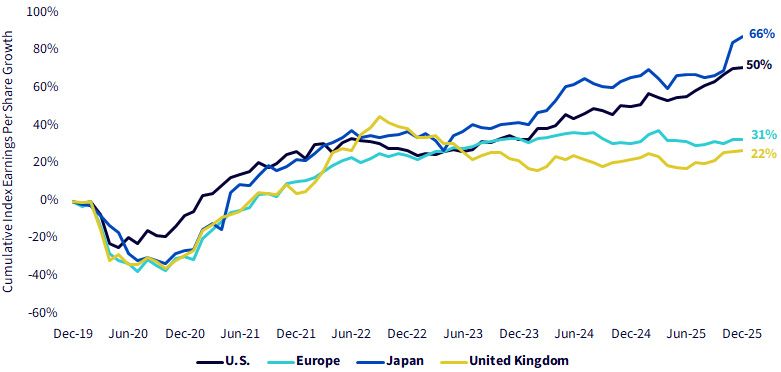

Since December 2019, trailing earnings per share for the MSCI USA Index, the MSCI EMU Index, the MSCI Japan Index, and the MSCI United Kingdom increased, with the MSCI Japan Index leading the pack, rising by 66%, outpacing its developed international peers. Notably, during the most recent earnings season in November, Japan's index-level aggregate earnings per share (EPS) recorded a sharp 9% jump, reflecting a concentrated wave of realized earnings gains.

Source: WisdomTree, FactSet from 12/31/19 to 12/31/25. Forward operating earnings is measured as a combination of actual and estimated earnings. You cannot invest directly in an index.

In contrast to U.S. earnings growth in 2025, which remained heavily concentrated among large technology and AI-linked companies such as Nvidia and the rest of the Magnificent Seven, Japan's second-quarter earnings strength was far more broad-based. Japanese companies delivered robust growth across multiple sectors, spanning traditional value areas such as utilities and materials as well as growth-oriented segments including information technology and communication services. This breadth of realized results is consistent with the pronounced late-2025 spike in Japan's trailing index-level EPS.

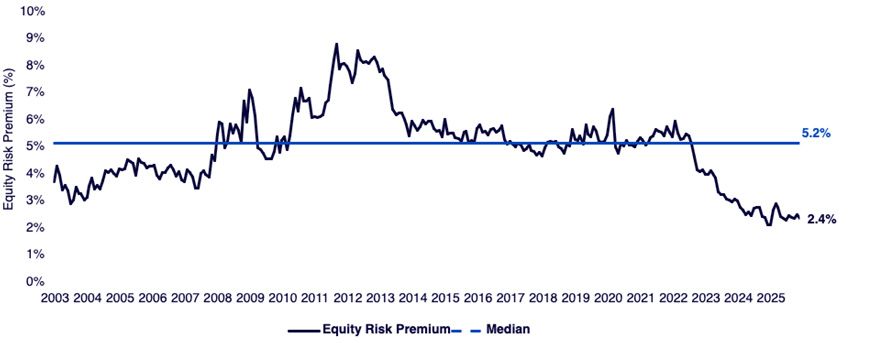

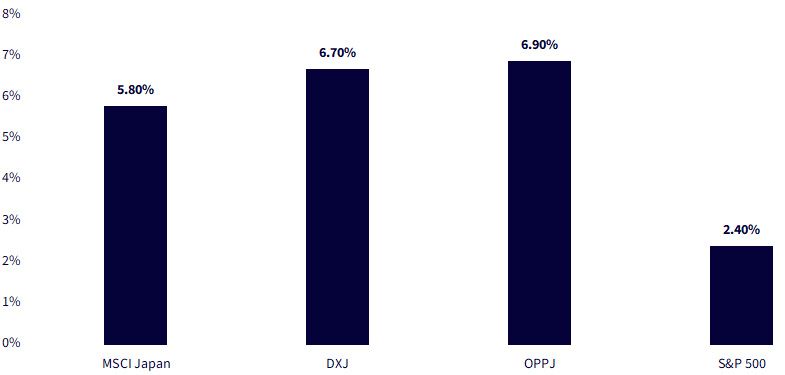

The equity risk premium that compares earnings yields to inflation-adjusted bond yields is our preferred gauge for comparing stocks and bonds. The U.S. equity risk premium currently sits below 2.5%—roughly half its average level over the last 20 years due to equity market gains as well as the normalization of bond yields. The over 5% equity premium we averaged over last two decades was well above the long-term equity risk premium we've observed in historical data.

Source: WisdomTree, FactSet as of 12/31/25.

Yes, Japanese bond yields have ticked higher. However, when comparing equity earnings yields with inflation-adjusted bond yields, Japan's equity risk premium remains more than twice that of the S&P 500. Under WisdomTree's valuation-sensitive approach, we estimate an equity risk premium closer to 7% for both the WisdomTree Japan Hedged Equity Fund (DXJ) and the WisdomTree Japan Opportunities Fund (OPPJ).

Source: WisdomTree, FactSet, as of 12/31/25. You cannot invest directly in an index.

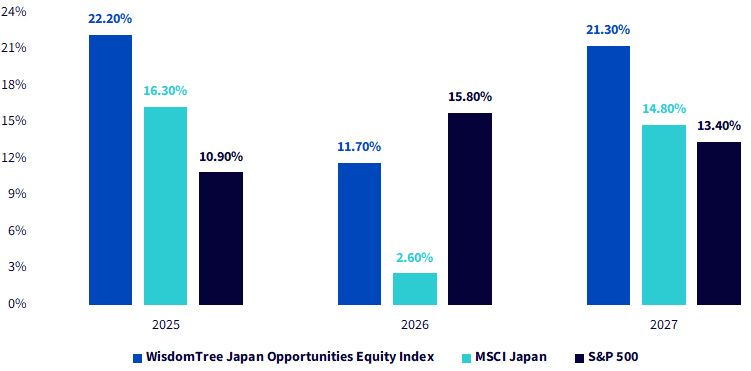

Looking ahead, analyst estimates through 2027 point to a stronger earnings growth outlook for the WisdomTree Japan Opportunities Equity Index relative to the MSCI Japan Index and the S&P 500.

Source: WisdomTree, FactSet as of 12/31/25. Forward operating earnings is measured as a combination of actual and estimated earnings. You cannot invest directly in an index.

It is rare to find a combination of relatively lower valuation ratios and even stronger upside earnings growth, a dynamic mix that creates a powerful and compelling case for the Japan "opportunity" as we see it.

Continue the Conversation

Hear directly from our thought leaders during our upcoming Office Hours on February 11 at 1 PM ET, “Japan’s Moment: Elections, Flows & Global Opportunities,” as they unpack what recent elections, market flows and global rotations could mean for Japan-focused strategies. Register here.

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Japan Hedged Equity Fund

Global Chief Investment Officer

Jeremy Schwartz has served as our Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Wharton Business Radio program Behind the Markets on SiriusXM 132. Jeremy is a member of the CFA Society of Philadelphia.

Director, Fixed Income

Behnood Noei serves as Director of Fixed Income at WisdomTree Asset Management, where he develops the firm’s suite of fixed income and currency exchange-traded funds and enhances existing investment processes. Behnood has 11 years investment experience in portfolio management and quantitative research. Prior to joining WisdomTree in 2022, Behnood was a portfolio manager and developer of some of the fixed income ETFs at J.P.Morgan Asset Management, where he was directly responsible for managing more than 7 Fixed Income ETFs and multiple SMAs with more than $13Billion in assets. He graduated from The Ohio State University with Master of Science degree in Finance and is a CFA charter holder.