The Power of Framing a Story in Investing

Published December 16, 2025

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- As of November 2025, the WisdomTree Japan Hedged Equity Fund (DXJ) has outperformed the S&P 500 over the past one-, three- and five-year periods while trading at significantly lower valuation multiples.

- Despite Japan’s reputation for stagnation, structural corporate reforms and a renewed focus on dividends and buybacks have made Japanese equities a global value opportunity hiding in plain sight.

- With a total shareholder yield of 4.6% and valuations well below U.S. peers, DXJ offers investors exposure to Japan’s corporate resurgence while neutralizing currency risk.

How we tell a story often matters more than the facts themselves. The same investment data can evoke wildly different reactions depending on the frame through which it's introduced. Investors, for all their spreadsheets and models, are still human, wired to respond emotionally to narratives, not just numbers. In a world where storytelling drives markets as much as earnings do, the way a strategy is presented can determine whether it's met with curiosity or dismissal.

Imagine hearing about an investment strategy that, as of November 26, 2025, has outperformed the S&P 500 Index over the past one, three and fiveyears and still trades at a significant valuation discount to that same benchmark. Most investors would likely want to know more, perhaps wondering what innovative U.S. sector or value methodology has managed that feat. Now, imagine if I told you this same description refers to a non-U.S. developed market equity strategy. Some enthusiasm might cool, replaced by skepticism or even disinterest.

That shift in perception reveals a deep homebias among U.S. investors, shaped by a decade of extraordinary domestic performance.1 The moment we reframe the same set of data as "Japan's equity market," emotional priors take over: images of demographic headwinds, deflation or slow growth may surface. Yet when we look purely at the facts—recent performance, earnings strength and valuation—Japan stands out as one of the most compelling large-market opportunities globally, and we will show some of these details in the figures that follow. This isn't just a story about Japan; it's a story about how narrative framing can obscure or illuminate opportunity.

Accessing Japan's Equity Story

At WisdomTree, our flagship strategy for accessing this opportunity is the WisdomTree Japan Hedged Equity Fund (DXJ),2 a vehicle designed to capture the performance of Japan's globally competitive exporters while neutralizing the currency fluctuations that often distort returns for U.S.-based investors. DXJ focuses on dividend-paying Japanese companies that derive a large share of their revenues from overseas markets. The result has been a strategy that, as of November 26, 2025, has outperformed the S&P 500 over the one-, three- and five-year periods, yet still trades at a meaningful valuation discount. For investors willing to look past the narrative and focus on the fundamentals, DXJ represents not just a Japan story, but a disciplined approach to capturing one of the most underappreciated equity opportunities in the developed world.

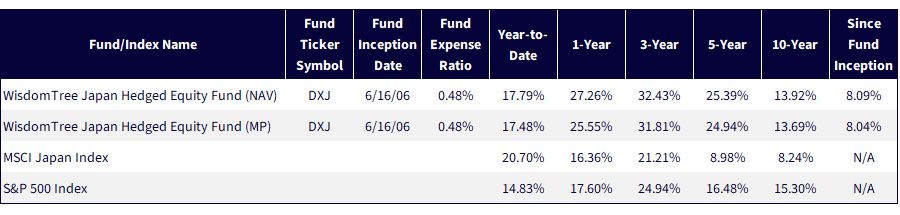

Figure 1: Standardized Performance

Sources: WisdomTree, FactSet; specifically, data from the Fund Comparison Tool in the PATH suite of tools, accessed 10/21/25, with returns as of 9/30/25. NAV denotes total return performance at net asset value. MP denotes market price performance. You cannot invest directly in an index. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click here.

The Outperformance of Japan That Many Do Not Realize

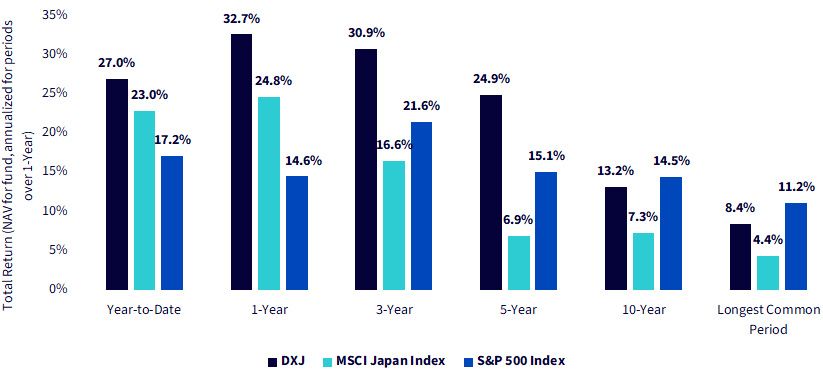

At first glance, few investors would expect Japan's equity market, long stereotyped as stagnant, to have outpaced the S&P 500 Index across any key time horizons. Yet that's precisely what the data shows. Neutralizing currency effects was important. The result, as shown in figure 2, challenges investors' intuitions: when stripped of narrative bias, Japan looks less like a laggard and more like a quiet outperformer.

Figure 2: When the Data Tells a Different Story: DXJ Quietly Outran the S&P 500 Index over the Year-to-Date, 1-Year, 3-Year and 5-Year Periods

Sources: WisdomTree, FactSet; specifically, data from the Fund Comparison Tool in the PATH suite of tools, accessed 11/28/25, with returns as of 11/26/25. The Longest Common Period references DXJ's 6/16/06 inception date. NAV denotes total return performance at net asset value. MP denotes market price performance. You cannot invest directly in an index. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click here.

Revisiting Valuation in an AI-Dominated Market

Valuation has quietly become one of the most polarizing topics in global equity investing. With the U.S. market at record highs, headlines increasingly ask whether AI is a bubble, a narrative fueled by extraordinary gains among a handful of mega-cap technology names.3 We don't expect investors to abandon U.S. equities en masse: structural innovation and capital depth remain undeniable strengths. But it's also true that when euphoria dominates attention, fundamentals can fade from view. We believe this is precisely when disciplined investors should re-anchor on valuation and total shareholder return, the combination of dividends, buybacks and cash flow generation that ultimately drives equity performance.

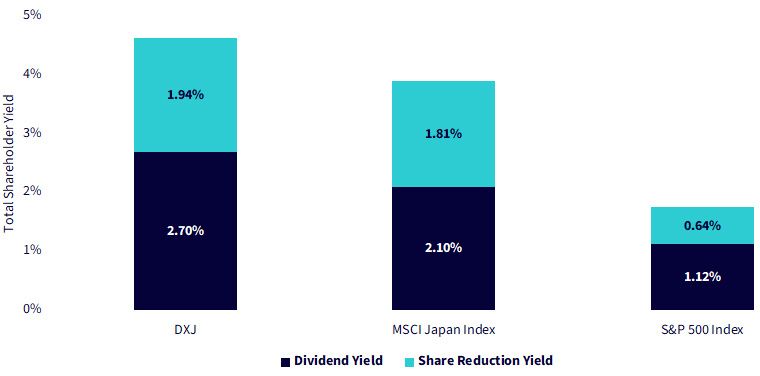

A Clear Valuation Gap

Figures 3a and 3b tell that story clearly. On total shareholder yield, Japanese equities, and particularly DXJ, offer a powerful contrast, as shown in figure 3a. Japanese companies have undergone a profound cultural and structural shift, prioritizing capital efficiency, dividends and buybacks in ways that would have been unthinkable a decade ago. Investors who still picture Japan as a low-return, cash-hoarding market are looking at an outdated snapshot.

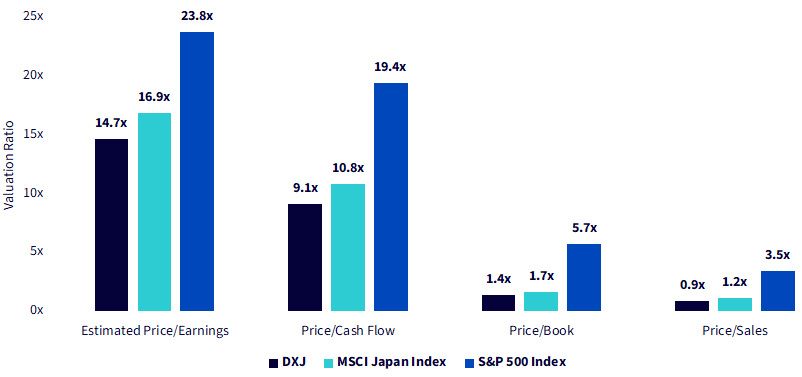

Fundamentals at a Fraction of the Price

On valuation multiples, the gap is even starker. Price-to-book and price-to-sales ratios tell the same story: Japan is still available at less than one-quarter of U.S. market valuations. Importantly, these discounts exist despite superior recent performance and improving corporate fundamentals. The implication is striking: investors can access companies benefiting from strong global demand, disciplined governance and rising shareholder payouts, all at valuations that the U.S. market hasn't offered in years.

Figure 3a: Japan's Corporate Renaissance: Higher Dividends and Buybacks Than the U.S.

Sources: WisdomTree, FactSet and Morningstar. Data as of 10/31/25. Subject to change. You cannot invest directly in an index. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here. To download the Fund prospectus, here. For definitions of terms in the chart above, please visit the glossary.

Figure 3b: A Market Still on Sale: Japan's Equities Trade at Deep Discounts to the U.S.

Sources: WisdomTree, FactSet and Morningstar. Data as of 10/31/25. Subject to change. You cannot invest directly in an index. For definitions of terms in the chart above, please visit the glossary.

Conclusion: Seeing beyond the Narrative

Markets don't just price earnings; they price stories. For more than a decade, U.S. equities have enjoyed one of the greatest narratives in financial history: innovation, dominance and resilience. But narratives can also blind investors to equally compelling stories unfolding elsewhere. Japan's equity market today combines global competitiveness, corporate reform, strong earnings growth and disciplined capital return, all at valuations the U.S. hasn't seen in years.

The data make the case clear: whether measured by performance, yield or valuation, Japan no longer fits the "perpetual laggard" narrative. Through DXJ, investors can access this transformation directly, harnessing Japan's improving fundamentals while neutralizing currency noise.

In investing, perception often lags reality. The opportunity lies in bridging that gap, recognizing when an old story no longer describes the world as it is. Japan is no longer the market it used to be; it may be the market investors least expect but most need.

1 Source: S. Lei and A. M. Mathers, "Familiarity bias in direct stock investment by individual investors," Review of Behavioral Finance, 16 number 3 (2024): 551–579.

2 DXJ is designed to track the total return performance, before fees and expenses, of the WisdomTree Japan Hedged Equity Index. This strategy focuses on export-oriented Japanese companies that pay dividends, and eligible constituents are weighted based on their cash dividends paid. The strategy also neutralizes the impact of the yen vs. U.S. dollar exchange rate.

3 Sources: K. Chan and M. O'Brien, "Is there an AI bubble? Financial institutions sound a warning," ABC News, 10/8/25; P. Carvão, P. "Is AI a boom or a bubble?" Harvard Business Review, 10/16/25; "‘Of course it's a bubble': AI start-up valuations soar in investor frenzy," Financial Times, 10/16/25.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.