WTPI

Equity Premium Income Fund

Published September 5, 2024

U.S. Head of Research

Since lows set during the pandemic, the S&P 500 Index has compounded at 25% per year. With the exception of 2022, drawdowns have tended to be shallow and manageable. Put another way, most investors have been penalized for making any change to their asset allocation. But what if markets were to take a pause from the all-time highs set on July 16? In our view, the WisdomTree PutWrite Strategy Fund (PUTW) could be the ideal strategy for flat-to-down markets.

The Fund sells put options on the S&P 500 in order to generate premiums of 2.5% per month. Should the market stay flat over the next year, it would be possible to generate returns of 30% (2.5% x 12 months). In exchange for the premiums, an investor sacrifices some upside potential should the market rally, and they could also experience losses should the market sell off. However, due to the Fund’s mechanics, you would expect to outperform the market by 2.5% per month on the downside.

While the following analysis has the benefit of hindsight in knowing that the market did not continue higher over the period, put writing gives investors the opportunity to limit their beta exposure to the market, in effect reducing drawdowns while still maintaining some correlation to the market should markets potentially churn higher. Should the frequency (or magnitude) of drawdowns increase, investors benefit by collecting higher extrinsic value from the options’ positions.

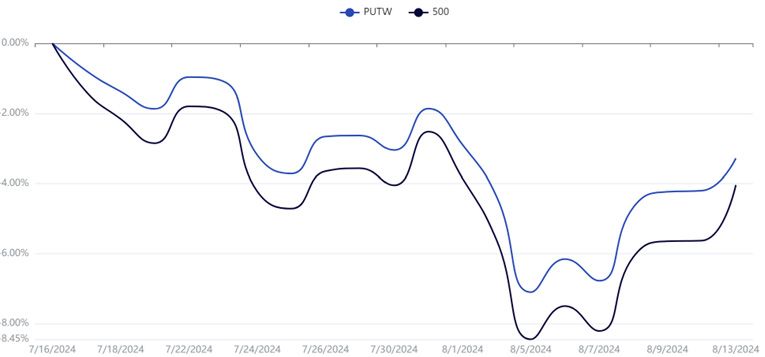

Source: WisdomTree, as of 8/20/24. 500=S&P 500 Index. Performance is historical and does not guarantee future results. Current

performance may be lower or higher than quoted. Investment returns and the principal value of an investment will fluctuate so

that an investor’s shares, when redeemed, may be worth more or less than their original cost. For the most recent month-end

performance, click here.

Since July 16 of this year, markets have generally trended lower, with the sell-off accelerating in early August when U.S. labor markets started to show signs of cooling. While markets have rebounded from the lows, PUTW has maintained the return advantage it experienced during the sell-off.

Source: WisdomTree, as of 11/24/23. Performance is historical and does not guarantee future results. Current performance may be lower

or higher than quoted. Investment returns and the principal value of an investment will fluctuate so that an investor’s shares, when

redeemed, may be worth more or less than their original cost. For the most recent month-end performance, click here.

Entering Q3 2023, there was also concern that market fundamentals might have started to show signs of age after a rapid increase in prices in 2023. While volatility was comparatively low entering this period, the fact that PUTW targets a 2.5% premium meant that the strategy really started to shine versus the S&P 500 Index as markets trended lower. While we know that markets ultimately recovered, PUTW outperformed by nearly 300 basis points to the lows, helping investors remain invested. After touching the lows at the end of October, the AI trade appeared to be back on as markets quickly rallied to all-time highs. While performance eventually eclipsed the returns of PUTW for this period, there was no guarantee that markets would not continue to be volatile.

Source: WisdomTree, as of 12/12/23. Performance is historical and does not guarantee future results. Current performance may be

lower or higher than quoted. Investment returns and the principal value of an investment will fluctuate so that an investor’s shares,

when redeemed, may be worth more or less than their original cost. For the most recent month-end performance, click here.

In what ended up being an extremely challenging year for U.S. equities, 2022 presents a textbook case for PUTW in action. During this time, traditional hedges like fixed income failed to offset losses in equity markets. During the initial downdraft, PUTW outperformed the S&P 500 Index by approximately 10%. Since markets remained volatile, PUTW was able to compound this advantage throughout the year, ultimately outperforming to the upside even as markets ground higher into 2023, albeit with lower volatility.

In the case of equities, it’s pretty straightforward—changes in prices plus dividends equal total returns. For PUTW, investor capital is invested in U.S. Treasury bills, which accrue interest linked to U.S. short-term interest rates. Additionally, the strategy targets a 2.5% premium from selling put options. When volatility is high, investors can benefit by selling options that are closer to at the money. During periods of lower volatility, PUTW sells options that are slightly in the money to achieve its income objective.

While equities have delivered strong returns recently, there is no guarantee that the Goldilocks period of high returns and historically low volatility will continue. In our view, a strategy like PUTW could add significant value to investor portfolios should markets remain volatile and/or rangebound.

There are risks associated with investing, including possible loss of principal. The Fund will invest in derivatives, including S&P 500 Index put options (“SPX Puts”). Derivative investments can be volatile, and these investments may be less liquid than securities, and more sensitive to the effects of varied economic conditions. The value of the SPX Puts in which the Fund invests is partly based on the volatility used by market participants to price such options (i.e., implied volatility). The options values are partly based on the volatility used by dealers to price such options, so increases in the implied volatility of such options will cause the value of such options to increase, which will result in a corresponding increase in the liabilities of the Fund and a decrease in the Fund’s NAV. Options may be subject to volatile swings in price influenced by changes in the value of the underlying instrument. The potential return to the Fund is limited to the amount of option premiums it receives; however, the Fund can potentially lose up to the entire strike price of each option it sells. Due to the investment strategy of the Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Equity Premium Income Fund

U.S. Head of Research

Bradley Krom joined WisdomTree as a member of the research team in December 2010. He is involved in creating and communicating WisdomTree’s thoughts on global markets, as well as analyzing existing and new fund strategies. Prior to joining WisdomTree, Bradley served as a senior trader on a proprietary trading desk at TransMarket Group. Bradley is a graduate of the Wharton School, University of Pennsylvania.